The clean energy giants are uniting their home batteries and smart thermostats to help tech giants power booming, AI-driven data centers without crushing the grid.

The leading U.S. providers of rooftop solar, home batteries, and grid-responsive smart thermostats have combined forces to create what could be the country’s biggest virtual power plant — or, more precisely, a lot of VPPs in data center hot spots.

On Wednesday, Sunrun, Tesla, and Renew Home announced an agreement to “deliver more than 16 gigawatts of flexible energy capacity” to tech giants and utilities around the United States. Those gigawatts will be produced by hundreds of thousands of home battery systems managed by Sunrun and Tesla, as well as more than 8 million smart thermostats and devices managed by Renew Home.

These batteries and smart thermostats are already installed in homes and businesses across the country, Paul Dickson, Sunrun’s president and chief revenue officer, told Canary Media. Some are enrolled in utility or grid programs that call on batteries to discharge, or thermostats to turn down energy use, during the handful of hours per year when grid demand is at its peak, he said.

But he noted, “Most of the constructs for these distributed power plants are tapping into the resources a fraction of the time they could be realized.” This new partnership is meant to “further legitimize these devices as core dispatchable, capable resources.”

Wednesday’s announcement is just the latest — and biggest — proposal for solving the country’s rising energy costs and grid congestion challenges through the power of distributed energy.

The aggregated energy-injecting and load-shifting capacity of batteries, smart thermostats, electric vehicle chargers, and remote-controllable appliances such as water heaters could add 80 gigawatts to 160 gigawatts by 2030, or roughly three to five times what’s now available across the country, according to analysis from the U.S. Department of Energy. VPP deployment at that scale could save U.S. utility customers about $10 billion in annual grid costs, the DOE estimated.

To make that happen, VPP companies need to coordinate with — and convince — utilities, regional grid operators, and state and federal regulators that distributed energy resources can do the work of traditional power plants. That’s easier said than done. The grid has been designed to deliver electricity from central power plants, not to rely on thousands of customer-owned devices turning on and off in unison to keep supply and demand in balance.

But traditional ways of managing the grid are falling short in the face of booming demand from the massive data centers that tech giants like Amazon, Google, Meta, Microsoft, and Oracle are building to fulfill their artificial intelligence ambitions. Some states are already seeing big spikes in energy costs due to data center growth. Across the country, lawmakers and regulators are demanding that developers of these facilities find ways to finance their own energy resources to avoid pushing more costs onto everyday consumers.

That’s putting pressure on tech giants to pursue novel approaches, from shifting when they use power, in order to avoid stressing the grid during times of peak demand, to investing in VPPs that can do the same work.

Home batteries and thermostats obviously can’t power data centers around the clock, Dickson said. But they can “solve elegantly for your peak-capacity needs, which is the bottleneck for data centers getting connected,” he said. “We want to provide for getting more data centers online in a way that doesn’t strain the grid or cause costs for customers to rise.”

Sunrun, Tesla, and Renew Home have a lot of existing customers to work with. Sunrun and Tesla already operate hundreds of megawatts of battery-based VPP capacity, including large-scale aggregations in California, New England, Texas, and Puerto Rico. And Renew Home — a spinoff of Google Nest’s smart-thermostat energy-shifting service Nest Renew and California startup OhmConnect — has partnered with major energy retailer NRG Energy to aggregate a gigawatt of flexible capacity in Texas, and is working with utilities in Arizona and other states.

Lots of companies are promising similar solutions. Voltus, a major U.S. demand-response and VPP aggregator, launched its “bring-your-own-capacity plan” last year, targeting tech giants struggling to interconnect to overburdened power grids. Earlier this month, Voltus and Google announced plans to develop 100 megawatts of this distributed capacity as part of the tech giant’s broader efforts to finance new energy resources for its expanding data center footprint.

Data centers want to “lock in that capacity, which is important to them,” Voltus’ CEO Dana Guernsey told Canary Media in early June. “They’re giving us the right signals to build, which we can take to our customers to save them money. And it’s not putting the cost on the ratepayers.”

The more data centers are willing to pay for VPP capacity, the more companies can offer customers to participate in them, Dickson said. Sunrun and Renew Home have paid out nearly $70 million to customers participating in existing grid-services programs, he added.

Low-income households could particularly stand to benefit if these programs prioritize these customers, according to a recent study by consultancy Brattle Group for the Natural Resources Defense Council. It found that if programs directed energy efficiency and VPP investments from data centers to lower-income customers in four cities — Atlanta; Memphis, Tennessee; Kansas City, Missouri; and Columbus, Ohio — participating households could save from $50 to more than $1,000 per year on their utility bills.

It’s not yet clear how Sunrun, Tesla, and Renew Home might deliver additional savings to customers at large. The companies didn’t disclose which existing or in-development VPP programs or data center opportunities they’re jointly pursuing.

But they are staking claims in key markets, including northern Virginia’s “Data Center Alley,” where massive data center expansions are pushing the grid to its limit, driving lawmakers and regulators to explore policies to limit cost and environmental impacts. Sunrun, Tesla, and Renew Home claimed they collectively have “more than 300 megawatts of capacity readily available for immediate deployment” in the region, which they expect will grow to at least 500 megawatts by 2030.

Sunrun, Tesla, and Renew Home also intend to provide VPP capacity to PJM Interconnection, the country’s biggest energy market, where power costs are spiking because of new data centers and PJM’s inability to bring new generation resources online. Specifically, the companies plan to commit capacity to PJM’s upcoming reliability backstop procurement, which is being designed to encourage data center developers to pay for new resources to match their grid impacts.

Renew Home has a lot of smart thermostat–equipped customers in the 13 states and Washington, D.C., region who are served by PJM but aren’t yet enlisted in VPP programs, CEO Ben Brown told Canary Media. “We have over a gigawatt of capacity in the ground, installed, flexing every day, providing savings for customers every day,” he said.

Last year, Renew Home ran tests of the potential grid relief those thermostats could provide, and found that customers were able to reduce summertime peak demand by about 380 megawatts over three consecutive afternoons, he said. That represented a little less than half its available “fleet” of customers, he added.

Dickson highlighted other parts of the country where the three companies have capacity to spare. According to the partners’ calculations, they can collectively relieve grid stresses for roughly two hours at a time by about 4.7 gigawatts in California, about 1.7 gigawatts in Texas, and about 1 gigawatt across Illinois and Ohio.

The number of home batteries and smart thermostats available for future service could expand if data centers are willing to pay more for these services, Dickson said. “Unlike a traditional power plant, this number grows every single day.”

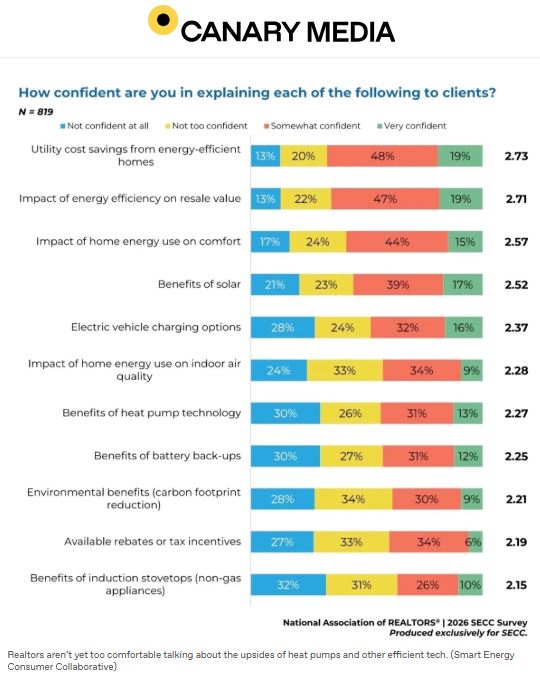

A new report finds that mentioning all-electric heat pumps in real estate listings delivers a sales premium. But most agents don’t note the appliance.

Would you pay more for a home with a heat pump?

You can bet I would.

I’d gladly fork over more money to bypass a gas or oil furnace, which — unlike an all-electric heat pump — spews toxic combustion by-products, runs the risk of poisoning my family with carbon monoxide, and contributes to climate change. And while heat pumps, which provide both heating and cooling, typically cost more upfront than conventional furnaces, they’re two to four times as efficient, and so could save me money in the long run.

Apparently, I’m not alone in prizing the comfort, safety, and economic benefits of these appliances.

Heat pumps give home values a boost, according to a new report by the nonprofit Smart Energy Consumer Collaborative, which studies consumer behaviors, interests, and concerns in the energy transition; 257, a customer-intelligence platform that profiles U.S. residential property characteristics for contractors, utilities, and others; and the trade group the National Association of Realtors. Their analysis showed that homeowners who install a heat pump can recoup up to a quarter of its cost just by mentioning it in real estate listings when they’re ready to sell.

While some homeowners may invest in a heat pump for its environmental bona fides, for most people, economics trumps all, said Scott Rosenberg, a co-founder and CEO of 257. “A homeowner who puts a garage on, redoes their bathroom, improves their kitchen, always thinks, ‘Am I going to get this value back?’”

By analyzing more than half a million sales of U.S. homes with ducted heat pumps from 2024 to 2025, the authors found that those with real estate listings mentioning the heat pump typically enjoyed a sales price boost of 0.6% to 1% over homes that didn’t advertise their efficient appliance. This modest lift translates to $2,300 to $3,900 per home, given a median sales price of $399,000.

“Just shy of $4K doesn’t sound like a lot of money on a home sale,” Rosenberg said. “But it’s actually a meaningful piece of the investment that you made to get the heat pump in the first place.”

In 2026, a ducted heat-pump system costs on average about $15,400, per energy marketplace EnergySage — though prices vary wildly depending on the region, a home’s size and electrical service, and local contractors, to name a few variables. A comparable gas furnace plus central AC system can cost half that, according to home services platform Angi. Mentioning a home’s heat pump in the sale listing, assuming the appliance cost around the average price, can recoup about 15% to 25% of the outlay.

Now, every home is different, and people willingly pay premiums for a wide variety of attributes, such as the floor plan, the views, and neighborhood vibes.

But Rosenberg is confident that when it comes to real estate listings, the heat-pump price bump is real, because of the approach his team used and the sheer amount of data they analyzed. 257 used a machine learning technique to cluster homes across hundreds of attributes to identify those that are nearly identical, he said. Then within those clusters, sales prices were contrasted for those homes where the heat pump was or wasn’t mentioned in the listing.

Yueming “Lucy” Qiu, an economics professor at the University of Maryland, called the report “very valuable” for helping to gauge the premium that people place on heat pumps. “I’m actually very happy that this came out,” said Qiu, who investigated the matter years ago at a smaller geographic scale.

In 2020, Qiu and her colleagues published a peer-reviewed study in Nature Energy that looked at home sales across 23 states from 2000 to 2018 for whether the presence of a heat pump improved the property’s sale prices.

Notably, to control for differences between homes that could influence price, her team looked at individual abodes that sold both before and after a heat pump was installed. They then compared the differences in sales prices (adjusted for inflation) with those for homes that hadn’t gotten a heat-pump makeover. Residences with heat pumps sold for a 4% to 7%, or $10,400 to $17,000, premium on the $240,000 average home price.

That’s a much bigger boost than the latest report identifies, but that’s because the groups investigated different questions. Qiu’s team asked, What’s the value of a heat pump? Whereas 257 asked, Once a home has a heat pump, what difference does highlighting it in the real estate listing make?

“We weren’t trying to make the case for energy efficiency, but rather to study whether it’s valued once it’s there,” Rosenberg said.

Qiu would love to see a follow-up study in which Rosenberg and colleagues analyze a subsample of homes with the methods she used in her paper. “Just as a robust check to see if, using similar methods, they find a similar magnitude [to what] we do,” she said.

Homebuyers are asking real estate agents more frequently about energy-efficient upgrades — not only for environmental reasons “but also to control and maintain their monthly costs, like their utility bills,” said Matt Christopherson, director of business and consumer research at the National Association of Realtors.

Yet Realtors often struggle to convey the benefits of energy-efficient features to clients, according to the recent report, which looked at a range of technologies. More than half of Realtors surveyed said they were “not too confident” or “not confident at all” in their ability to explain the benefits of heat pumps.

Real estate agents are the ones writing the listings, Rosenberg pointed out. In homes with a heat pump, it was mentioned in the listing just 8% of the time.

If real estate agents become more aware that potential buyers are willing to pay more for homes with heat pumps, and they lean into promoting the appliances, Rosenberg believes “that’ll have a virtuous-cycle effect of reinforcing and signaling to buyers that this is something they should pay attention to.”

Of course, some of us are already keeping our eyes peeled for listings that give heat pumps and other clean energy perks a shoutout.

Industrial buildings could host gigawatts of shared solar to deliver low-cost power to underserved urban communities — if states and utilities allow it to scale up.

Natasha Keefer is not a fan of heights. But on June 5, Keefer, who heads the Energy Solutions team for the Americas for Prologis, one of the world’s largest logistics companies, braved the ladder up to the roof of a 147,500-square-foot warehouse in Oakland, California, to take a look at the latest solar project her team had built.

The 720-kilowatt array will generate far more power than the company’s warehouse can use. In fact, the building in East Oakland is vacant right now. But that’s OK, because as a community solar project, it’s feeding electricity directly into the grid, Keefer explained to a group of state and local officials who had gathered to “flip the switch” on the array.

Ava Community Energy, a public energy provider serving Oakland and other East Bay and Northern California communities, will buy that power and make it available to low-income households, with a guarantee for subscribers of at least 20% savings on monthly utility bills.

Half of U.S. states and Washington, D.C., have adopted policies enabling some kind of community solar program. Many such projects are built on open fields. But as one of the country’s largest owners of logistics real estate, Prologis is “looking to deploy solar on as many rooftops as we can,” Keefer said.

In a sense, warehouse rooftops are like open fields in dense urban landscapes, with acres of flat space available for solar panels.

Ava has awarded Prologis a contract to build nearly 7.3 megawatts of solar on sprawling roofs across five sites, enabling about 3,000 residents to see lower bills. Keefer previously worked for Clean Power Alliance, another California community energy provider, which is building 9 megawatts of warehouse-rooftop community solar with Prologis.

“California has a huge need for power. I’m not claiming distributed generation is the answer for all our needs,” she said. “But you need all the tools in your toolbox.”

Similar logic is driving U.S. states from the mid-Atlantic to the Midwest to expand opportunities for community solar on warehouses and other commercial and industrial buildings. There’s certainly a lot of roof space to go around, said Peter Light, CEO of Lumen Energy, which brokers deals between real estate owners and solar developers.

His company’s analysis of federal data indicates U.S. commercial, industrial, and institutional rooftops could host 581 gigawatts of solar, enough to provide the lower bounds of the country’s overall electricity demand. Similar data from a 2023 study by the Environment America Research and Policy Center found that warehouses across the U.S. have nearly 16.4 billion square feet of rooftop space, capable of hosting enough solar to power more than 19 million homes.

Of course, not all of that space can be used to generate solar power. But Light thinks that rooftops should be considered as valuable as open land for utilities and policymakers desperate to meet booming demand for electricity.

“With surging power prices from data centers and AI, and general electrification, utilities and states are asking, ‘Where can we get capacity now?’” he said. In many cases, rooftop solar systems can come online more quickly than utility-scale solar, which frequently faces yearslong interconnection studies and hefty grid upgrade costs, he said.

But only a fraction of available roof space is being used for solar today. Community solar can be a “revolutionary” tool to unlock that rooftop potential, Light said. “What community solar does is turn energy complexity into rental income — and new rental income is what real estate people understand,” he said.

Susan Uthayakumar, Prologis’ chief energy and sustainability officer, agrees that community solar is a valuable option for real estate owners.

Prologis has deployed more than a gigawatt of solar and batteries across its global real estate footprint, largely to pursue its sustainability goals, she said. That includes more than 300 megawatts of solar at its U.S. properties, more than any other U.S. real estate owner.

Some of that power is being used on-site, where the demand exists. But when it comes to warehouses, most have relatively low power needs. “We usually need only 30 to 40% of the roof space for on-building demand,” Uthayakumar said. “We like to contribute the rest of the space for community solar.”

Black Bear Energy, a subsidiary of real estate efficiency and sustainability contractor Legence, has more than a gigawatt of on-site solar projects in its development pipeline, with customers ranging from apartment buildings to office parks. But relatively few building owners have the capital and long-term ownership commitment to invest in and own solar projects, said Victoria Stulgis, Black Bear’s president.

What’s more, buildings that are rented or leased face the split-incentive problem: The owner is less likely to pay for the solar installation when tenants will be the ones reaping the benefits with lower electricity bills.

That’s why Black Bear Energy and customer LBA Logistics pursued tens of megawatts of community solar projects on warehouse rooftops in Maryland and in Illinois. “Community solar structures are much more attractive to us because we’re basically monetizing our rooftops,” said Michelle German, a vice president at LBA.

So what’s preventing more warehouse rooftops from being harnessed for community solar? First of all, it’s possible only in states with programs that allow shared solar.

Right now, that’s limited to Colorado, Illinois, Maryland, Massachusetts, New Jersey, New York, and a few other states, according to the Coalition for Community Solar Access, a trade group. Prologis is planning to build about 116 megawatts of rooftop solar in New Jersey with developer Solar Landscape, and another 82 megawatts across 45 rooftop projects in Illinois.

Second, states that do offer these programs restrict how much can be built, forcing developers and site hosts to scramble to design and bid projects into a limited pool of opportunities. But those pools are getting bigger. Earlier this year, New Jersey expanded its community solar program to 3 gigawatts, and Maryland is set to establish a 2-gigawatt target for distributed solar, including community solar, later this year.

But in California, community solar policy is moving in the opposite direction, its advocates say. State utility regulators have rebuffed a multiyear effort to expand community solar, leaving tight restrictions on how much can be built. Ava Community Energy’s 7.3-megawatt project portfolio with Prologis maxed out how much solar it could build under an existing program based on the number of customers it served in Alameda County — although its recent expansion into other parts of California have opened the opportunity to increase its portfolio by another 11 megawatts.

California regulators and utilities have argued that community solar projects are more expensive than utility-scale solar, making them a bad bet for keeping the state’s rising electricity costs in check. That’s because of both the economies of scale that giant solar farms offer and the extra costs of installing arrays on rooftops rather than on open land.

But that simple cost comparison doesn’t capture other benefits, Prologis’ Keefer said. “This is local to the community it serves,” she said. “It’s utilizing the existing built environment.” And because the power flows directly to existing urban power grids, “you don’t have to build a transmission line from the desert” to get the power where it’s needed.

In some states, community solar programs prioritize rooftops over empty fields. New Jersey limits projects almost exclusively to commercial and industrial rooftops, said Charlie Coggeshall, mid-Atlantic regional director for the Coalition for Community Solar Access. Similar requirements and incentives meant to prioritize solar development on buildings or “brownfield” sites like landfills exist in Illinois, Massachusetts, Maryland, New York, and other states, according to CCSA data.

Adding batteries to community solar systems could help them further reduce peak power demands in urban centers, according to research from consultancy Brattle Group commissioned by solar developer Solar Landscape. The analysis found that community solar-battery systems at commercial and industrial buildings in California could lower energy and grid costs more than “remote, ground-mounted projects,” mainly because they are situated in more densely populated areas.

Warehouses also tend to be located in communities that suffer from higher than levels of poverty and air pollution. A 2024 report led by researchers at Stanford University found that widespread deployment of commercial solar could provide disadvantaged communities significant relief from rising utility bills.

These are the kind of impacts that make urban community solar worth doing, said Rowena Brown, an Oakland City Council member and Ava board member. Residents of the East Oakland neighborhood that surrounds the Prologis warehouse “are unsure whether they can really benefit from lower energy costs — and they face real barriers to the clean energy transition,” she said. “I think of this project as a clear opportunity to show we care about the families here.”

Trump and GOP lawmakers revoked lucrative tax credits for rooftop solar. The results are predictable.

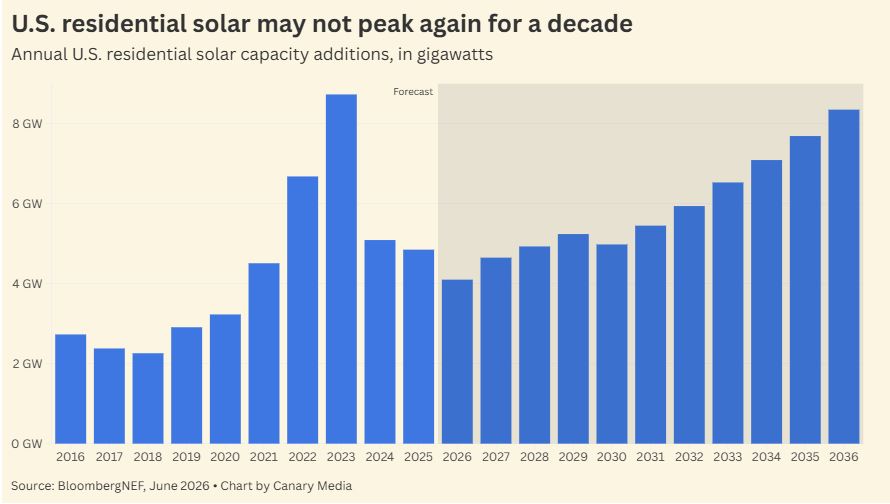

With solar panels getting cheaper each year and utility bills soaring, you might expect rooftop solar to be booming in the U.S. That’s not the case.

Instead, thanks in large part to the Trump administration’s revocation of federal tax incentives, residential rooftop solar installations in 2026 are expected to fall to their lowest level since 2020, per new BloombergNEF data.

Nearly one year ago, President Donald Trump signed the One Big Beautiful Bill Act into law and eliminated a 30% federal tax credit for rooftop solar systems. It was a major blow to an industry that was already struggling because of high interest rates, tariffs, and a seismic policy change in California, the state that has led the nation on rooftop solar adoption. The legislation also eliminated the 30% tax credit that applied to battery backup systems, which homeowners increasingly pair with photovoltaics.

Yanking away tax credits makes it costlier to install rooftop solar, so it’s no surprise the move dampened sales. People who buy rooftop solar systems are mainly looking for relief from high utility bills, and solar installations are already more expensive in the U.S. than in many other countries. Residential solar costs $2.58 per watt, on average, compared with around $1 per watt in Australia, a global leader in the space.

The outlook isn’t great. BNEF analysts think it will take more than a decade for the industry to match the installations record it set back in 2023. To be fair, that record happened under some very specific circumstances: The Inflation Reduction Act, passed the previous year, had boosted the federal tax credit for rooftop solar, and, at the same time, Californians were sprinting to install systems before the state did away with its lucrative compensation scheme in April 2023.

Still, there are some glimmers of hope. In California, the residential solar market is set to rebound this year and grow by 17% from last year. Meanwhile, Florida, the No. 2 state for rooftop solar, is set to see its installations grow by a staggering 62% in 2026.

That suggests the biggest state markets for rooftop solar are fairly resilient. Some combination of ample sun, high awareness of solar, and rising utility bills has enabled the clean energy tech to keep growing even though a significant slice of homeowners already have their own panels.

Meanwhile, although its potential is much more modest, a far smaller and more accessible form of residential solar is sweeping the nation: balcony solar. Several states have passed legislation green-lighting these DIY plug-in solar systems. They can’t deliver the same wattage as a classic rooftop setup, but they’re relatively cheap and available to renters — not just homeowners. Maybe that emerging boom can help offset the bust for rooftop systems.

The startup’s first-of-a-kind geothermal project hit key milestones in Germany — but also technical hurdles. Now it’s looking for partners to help finish the job.

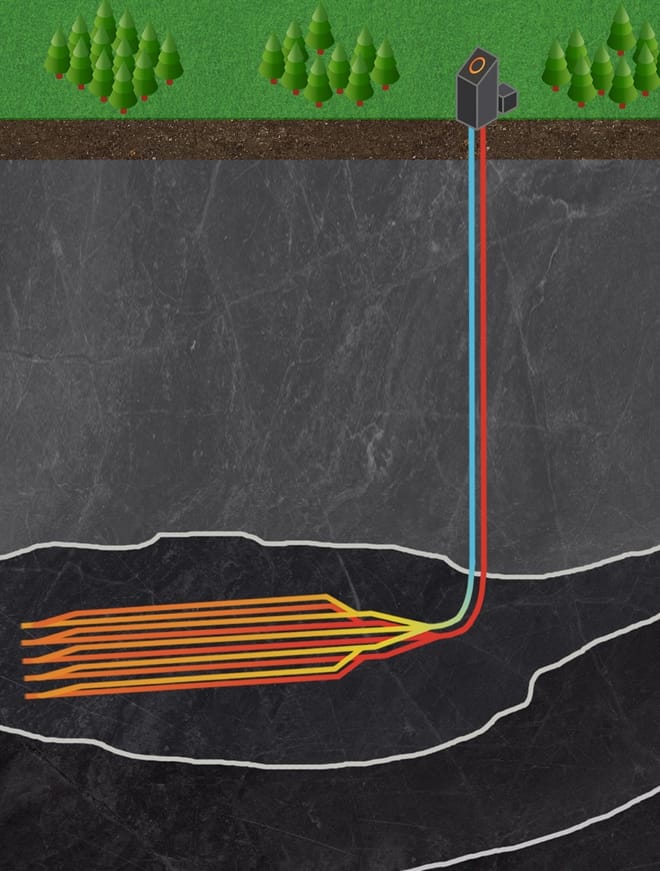

The startup Eavor Technologies hit a crucial milestone late last year when its flagship geothermal project — a novel closed-loop system — started sending electricity to Germany’s grid. The company had completed the first of four planned loops, and it expected to start construction on its second loop earlier this spring.

Now, Eavor says it’s revising that timeline. The Canadian startup encountered major engineering challenges when drilling its initial wells deep underground near Geretsried, Germany. While Eavor was able to fix those issues, it’s seeking new project partners and investors to help it complete the next-generation geothermal system.

“We’re looking to make Loop 2 happen as soon as practical and in the best form that we can,” Matt Toews, Eavor’s co-founder and chief technology and operating officer, told Canary Media. “Exactly how that shakes out, I can’t say yet until it’s done.”

Still, “The overall grand plan stays the same,” he added. “It’s really about proving the technology, … coming down the learning curve, and going deeper and hotter” to unleash geothermal energy.

Eavor began drilling in Geretsried, which is south of Munich, in July 2023 after winning a grant for 91.6 million euros from the European Union’s Innovation Fund. At full scale, the project is intended to supply 8.2 megawatts of electricity to the grid or 64 MW of district heating to nearby towns.

Demand for the renewable resource is rising globally as countries look to boost supplies of clean, domestic energy, both to meet their soaring electricity needs and to reduce reliance on volatile fossil fuels. Traditionally, geothermal power plants have been confined to places with natural reservoirs of steam and hot water, like near Iceland’s volcanos or California’s thermal springs.

Eavor is one of dozens of companies trying to break those constraints by developing technologies that can access earth’s heat potentially anywhere — though the industry is just starting to deploy those solutions in the real world.

It’s not uncommon to see delays or evolving plans when rolling out new energy technologies.

Emily Pope, a geologist and senior fellow at the Center for Climate and Energy Solutions, said she wasn’t remotely surprised to hear that a first-of-a-kind project like Eavor’s encountered technical hurdles. Pope previously worked on the Iceland Deep Drilling Project, an ongoing research initiative to tap into superhot reservoirs, which hit significant snags after its first well unwittingly struck magma and then the second one collapsed.

“The setbacks [for Eavor] were real, but also understandable and predictable, and something that we see in every industry that is trying to grow,” she said, adding that geothermal developers in general “are going to have to learn by doing.”

Eavor’s approach is akin to building a massive radiator several miles beneath the earth’s surface. Each loop involves drilling two vertical wells and pairs of horizontal, or lateral, wells that stretch out like the tines of a fork. The wells are later connected underground and sealed off. As water circulates within the system, it collects heat from the rocks and brings it to the surface.

The basic concept is tried and true; this is essentially how shallow geothermal networks heat and cool homes and buildings. But Eavor’s system requires drilling far deeper, and in much trickier conditions, in order to provide utility-scale electricity and heating.

In the United States, another next-generation technology — an enhanced geothermal system, or EGS — has been gaining the most traction among developers. The startup Fervo Energy is building what will become the world’s largest EGS project in Utah, using fracking and horizontal drilling techniques to create artificial reservoirs. The first phase of this 500-megawatt project is set to start producing power this fall.

As a technology, enhanced systems are considered more advanced and relatively less costly than closed-loop systems for power generation. The loops are generally less efficient at extracting heat from the earth, since their fluids don’t directly touch rocks, and they can be lengthier and more complex to drill. But EGS has its own trade-offs: The approach carries the risk of inducing earthquakes and straining local water supplies, though experts say both issues can be mitigated.

“Closed-loop just leapfrogs over those challenges” because of its contained design, Pope said, adding that the systems could be a better fit for harnessing heat in dense urban areas and in water-scarce regions. In the U.S., the companies XGS Energy, GreenFire Energy, and Vero Geothermal are also pursuing closed-loop projects in places like California and New Mexico.

“There’s a demand for it, and there’s just a lot of good reasons to try to do it,” Pope said.

Last fall, Eavor released results from two years of activity in Geretsried, which showed how the company reduced drilling times and improved performance despite encountering challenges. In late May, Toews penned a technical update describing in greater detail the key problems Eavor faced in drilling its first loop.

After its first boreholes became unstable, leading to the risk of stuck pipes, Eavor changed the type of drilling-fluid system it used. Broken equipment and slow drilling speeds initially plagued the project, owing in part to the hard rock types and the length of the lateral wells. By tweaking its techniques and adapting equipment, Eavor said it cut its average drilling time by over 70% from the first four lateral well pairs to the last.

The company also developed an “active magnetic ranging” system to give it more precision when drilling long wellbores and getting its lateral well pairs to intersect underground. “If you look at the wells, the first ones are kind of like wet noodles, and the last ones are gun-barrel straight,” Toews said in an interview.

But one challenge proved harder to address.

Eavor began by using two drilling rigs in parallel to form the “motherbores” from which the lateral wells extend out. The company found that poor cement casing on the motherbores allowed fluid and mud to flow freely between the two rigs, which are supposed to be completely sealed off. So the team switched to using one rig at a time — a temporary fix that doubled the time and cost for Eavor’s first loop.

The startup initially planned to drill 12 pairs of lateral wells for that first loop. But it stopped short at six so that it could try again with proper cementing design on the second loop. This could mean bringing on project partners with more experience drilling multilateral wells. Pope noted that well leakage is a common engineering problem in the oil and gas industry — one that drilling teams can generally account for and address.

Today, the system is producing as much power as Eavor expected for a loop of that size: about half a megawatt. For Eavor, that’s proof the technology works as promised, though the firm hasn’t said when it expects to reach full capacity for electricity and district heating.

“Despite all the challenges we had, and by us solving them, it has served its purpose,” Toews said of the flagship project. “We’ve proven that we can extract heat with our system, we know what it costs, … and we know exactly how to build and operate these loops at commercial scale.”

Pope said she hoped that Eavor and other companies will continue to be transparent about their experiences, to help other developers avoid similar pitfalls and to manage public expectations.

“I think it’s really important for the industry broadly to understand where companies are in their technological development, so we can have honest conversations about how close we are to achieving a commercial-scale product,” she said.

Sky-high fossil fuel prices drove people around the world toward clean energy. But even as the Strait of Hormuz reopens, they may not turn back.

America’s war with Iran is maybe, possibly, headed for resolution, but its impact on the global energy sector isn’t fading anytime soon.

The U.S. and Iran signed a deal on Wednesday to end their three-month conflict and reopen the Strait of Hormuz, a crucial oil and gas shipping lane. It’s still unclear what the agreement exactly entails, or whether it’ll even hold up, but fossil fuel markets are taking it as a good omen. Global oil prices have already fallen to their lowest level in months, and gasoline prices across the U.S. are starting to sink. Still, experts say it could take up to a year for oil and gas prices to stabilize, especially given that Middle Eastern fossil fuel infrastructure was damaged during the war.

Amid these past few months of uncertainty, much of the world turned to a common solution: clean energy. People swapped gas cars for EVs, turned to electric appliances for cooking, and took other big — and potentially permanent — steps away from costly and volatile fossil fuels.

When 2026 started, the EV market wasn’t in a great place. The end of federal tax credits had tanked the U.S. market, and global sales were sluggish, too. But with skyrocketing fossil fuel prices came a renewed interest: New EV sales rose through April and May around the world, and BloombergNEF anticipates sales will climb even further throughout 2026.

Outside of higher prices at the gas pump, the U.S. hasn’t felt much of an impact from the energy shock. But in Europe and Asia, people are grappling with higher fuel costs for cooking, heating, and power generation, and have turned to clean solutions in response.

Instead of following President Donald Trump’s call to buy more U.S. fossil fuels, European Union leaders called for a bloc-wide shift to renewables. In Britain, Germany, and the Netherlands, tons of households installed rooftop solar arrays to avoid high electricity prices. In India, a cooking gas shortage led residents toward induction stoves. The Philippines similarly saw a surge in rooftop solar installs, and a new International Energy Agency report suggests the country and its neighbors across Southeast Asia will keep the clean investments coming given the region’s reliance on Middle Eastern oil and gas imports.

Time will tell if the war and its fallout prove to be an inflection point for the clean energy transition, but analysts with think tank Ember argue it’s certainly a possibility. After all, the oil crises of the 1970s pushed the world to look beyond the Middle East for fossil fuel supplies, and to pursue more efficient uses of oil and gas. The same thing could happen this time around — only with cleaner, cheaper, and more secure energy as the alternative.

Hot spring: Clean energy had a record-breaking spring in the U.S., with solar generation beating out coal for the first time in May, among other wins for solar, wind, and battery storage throughout the season. (Canary Media)

Clean energy’s next hurdle: Most wind and solar projects under construction in the U.S. have secured “safe harbor” status, meeting the July 4 deadline to tap federal incentives, but now developers must race to complete those projects in four years. (Canary Media)

Courts deliver on climate: Clean energy groups and states continue to fight the federal government’s multipronged blockade on wind and solar development, scoring victories as the Trump administration abandons one anti-wind fight and is ordered to release millions of dollars in climate grants revoked from states that voted for Kamala Harris in 2024. (E&E News, Utility Dive, New York Times)

Transmission disconnect: The New England Clean Energy Connect transmission line was supposed to bring tons of clean hydropower from Canada into the Northeast U.S., but energy imports have increased only a tiny bit since the line began running in January. (Canary Media)

Solar funding unplugged: The DOE has redirected tens of millions of dollars that the Biden administration allocated to Puerto Rico for a resilient network of solar panels and batteries toward building a gas pipeline and other fossil fuel infrastructure. (Grist)

Double-edged grid upgrades: Making much-needed upgrades to the U.S. grid could result in a $1 billion payout to American utility executives, as publicly traded utilities’ stock valuations are directly tied to their spending. (Reuters)

The flow has been stop and go for the first few months, but the line shows plenty of potential to boost Massachusetts’ renewable energy supply.

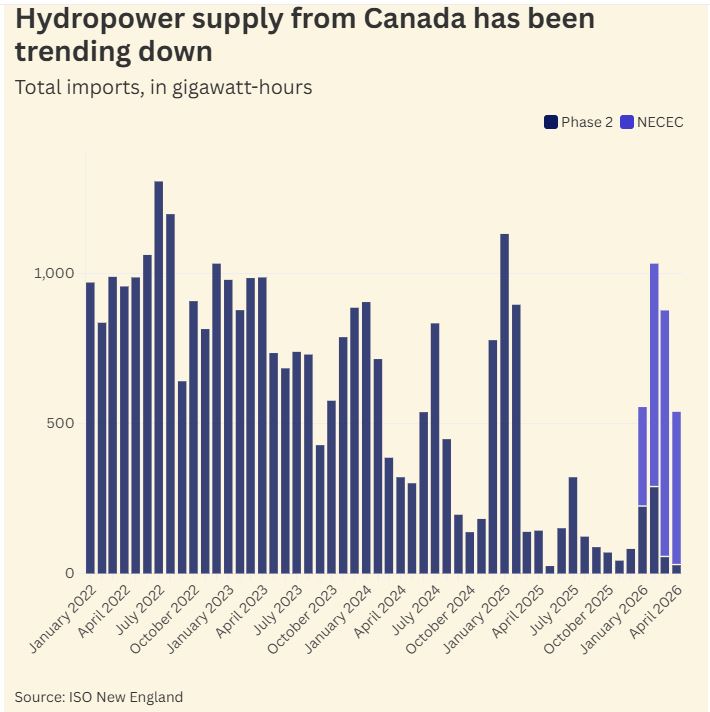

When the New England Clean Energy Connect transmission line started carrying electricity from Canada into Maine in January, supporters hailed the project as a triumph for renewable power. Now, after nearly six months of operations, the early numbers raise questions about whether the project will be able to advance the region’s energy transition as much as advertised.

Energy flow into New England is up just marginally, and there have been roughly 27 days when no power at all traveled along the new line, commonly called NECEC. If current trends hold, New England will receive less hydropower this year over two transmission lines than it did over just one line in 2023 and previous years.

“What we’ve seen so far is not what some people expected to see,” said Joseph LaRusso, manager of the Clean Grid Program at climate nonprofit Acadia Center.

Potentially putting further strain on the supply of Canadian hydropower is the Champlain Hudson Power Express, a transmission line that started sending electricity from Quebec into New York City this month.

NECEC has its origins in a 2016 Massachusetts law that required the state to procure 1.6 gigawatts of offshore wind power and another 1.2 gigawatts of additional renewable energy. The plan was to contract with state-owned Canadian power supplier Hydro-Québec to tap into the region’s abundant hydropower resources and build a new transmission line to carry the electricity south.

The first proposal — a 192-mile project through New Hampshire — was abandoned in 2019 after public outcry about the impact on the state’s forests. The transmission line through Maine faced similar controversy. In 2021, a statewide referendum vote put the project on hold until 2023, when a jury ruled that the development could be restarted.

Two and a half years later, NECEC came online and started carrying the first electrons into New England. It’s certainly a notable achievement in a time when the Trump administration has been doing all it can to stop progress on clean energy, including offshore wind — the cornerstone of the Northeast’s decarbonization plans. And although the results so far have been mixed, some see potential for the line to make a sizable impact on New England’s clean energy future.

When NECEC came online earlier this year, Massachusetts Gov. Maura Healey, a Democrat, and climate advocates touted it as a major win for the state’s renewable energy goals and a way to save residents money on their utility bills. Massachusetts contracted with Hydro-Québec for 9.55 terawatt-hours of hydropower per year, roughly 20% of the state’s annual electricity demand.

The operations have not had the smoothest start. NECEC was completely inactive for several spans — from a half day on April 28 to nearly two weeks at the end of May and beginning of June. The most recent outage was due to “technical difficulties,” Hydro-Québec spokesperson Lynn St-Laurent said in a written statement.

“Once repairs were completed, deliveries resumed,” she said. “With any new transmission infrastructure, a period of optimization and fine-tuning is to be expected.”

Still, most of the time, hydropower has flowed steadily on the new infrastructure. Through the end of April, Hydro-Québec exported about 2.4 terawatt-hours of power on the transmission line.

If the power is (mostly) moving as planned, why are some people still skeptical that the project will deliver the promised benefits? Because so far, it hasn’t done much to add to the total supply of renewable energy in New England.

Before NECEC, New England already imported significant amounts of hydropower on a transmission line known as Phase 2, which runs from Quebec into central Massachusetts. In 2019, the year the Massachusetts regulators approved the contracts between utilities and Hydro-Québec, more than 12 terawatt-hours traveled onto the New England grid over the line.

But starting in 2023, Hydro-Québec started selling less and less energy to New England over Phase 2. For nearly three weeks in early 2025, exports ceased entirely. Through the end of April this year, just over half a terawatt-hour has come south over that line. On paper, it can look a lot like NECEC isn’t allowing more energy into New England but is instead just giving it a new road to travel along.

“We’re not seeing much net new flows coming from our neighbors,” said Dan Dolan, president of the New England Power Generators Association. “We are running pretty close to the net energy flows we had in 2025, which were the lowest amount of imports that New England has ever gotten from Quebec.”

At the same time, Quebec has started importing power over the Phase 2 line, a rare occurrence before 2025. In the first four months of this year, more than 500 gigawatt-hours traveled into Canada on the line. Because New England’s electricity supply relies heavily on natural gas generation, the region is still burning fossil fuels to ship energy north even though it is receiving hydropower for its own use.

“We’re seeing a heavier natural gas burn on the rest of the generation fleet than I think many of those states had assumed going into this year,” Dolan said.

The main driver behind slowing exports seems to be the drought conditions that have lingered in Quebec for the past few years. During wetter periods, the hydropower industry uses large reservoirs to store water to help it ride out these drier times, said Gilbert Bennett, a senior adviser for WaterPower Canada, a hydropower trade group.

As generators wait for rainier days, their first obligation is to supply domestic customers, he said. That means there will likely be times when Hydro-Québec needs to import electricity over the Phase 2 line to offset some of the hydropower it is contractually obliged to send to Massachusetts over NECEC.

“Electricity flows between Québec and New England are dynamic and vary continuously based on market conditions and system needs on both sides of the border,” St-Laurent said.

Financially, New England customers should not be at risk from these ongoing shifts, LaRusso said. Massachusetts’ contract with Hydro-Québec includes provisions that require the Canadian company to pay financial penalties if it fails to deliver according to its contract.

“To the extent that imports are curtailed, Hydro-Québec is liable to make the electric utilities whole for the cost of replacement power,” LaRusso said.

It is less clear whether NECEC will boost Massachusetts’ renewable energy supply in the long run.

Still, the new transmission line has at times demonstrated its potential to help New England achieve a cleaner energy supply, LaRusso said. He pointed to May 16, a sunny day when solar power reduced demand on the grid and NECEC was going full tilt. Natural gas plants were running at low levels, and most of the power was heading to New York. For a short time, all the region’s power needs could be met by nonfossil fuel resources.

“Hypothetically, [grid operator] ISO New England could’ve turned off its gas generators,” LaRusso said. “It really gets you thinking of the resources available and how they could be managed and shared in the future.”

Bennett is also confident in the long-term outlook. In general, he said, climate change is forecast to create wetter conditions in Quebec. And the region is investing heavily in additional hydropower facilities as well as onshore wind. The years to come, he said, will bring plenty of renewable resources to share with Canada’s southern neighbors.

“Over the long term, we see a bright future,” Bennett said.

In California, Texas, and other places, solar, wind, and batteries hit new highs. Here are the big takeaways from this year’s shoulder season.

As spring gives way to summer, many parts of the U.S. are already feeling the heat. It’s a good moment to take stock of the energy breakthroughs that transpired this past “shoulder season.”

That’s the period of time between the chill of winter and the high temperatures of July and August, when renewable energy systems tend to perform best. With the milder weather and longer daylight hours, total demand stays relatively low while wind and solar ramp up, covering greater shares of grid consumption.

Here are four ways clean energy set new records this spring — and what these feats tell us about where the energy system is headed. While records reflect momentary successes amid ideal conditions, they’re worth noting because they push the boundaries of what’s possible, and lay the groundwork for similar success across broader swaths of the year.

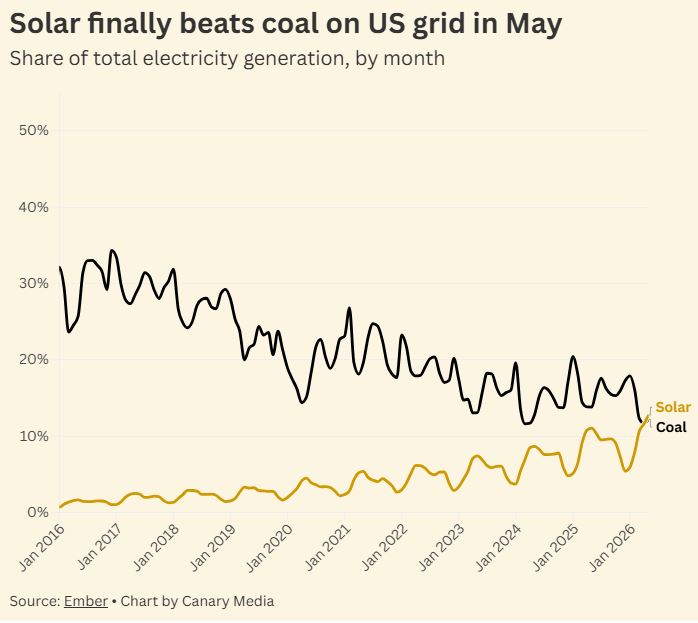

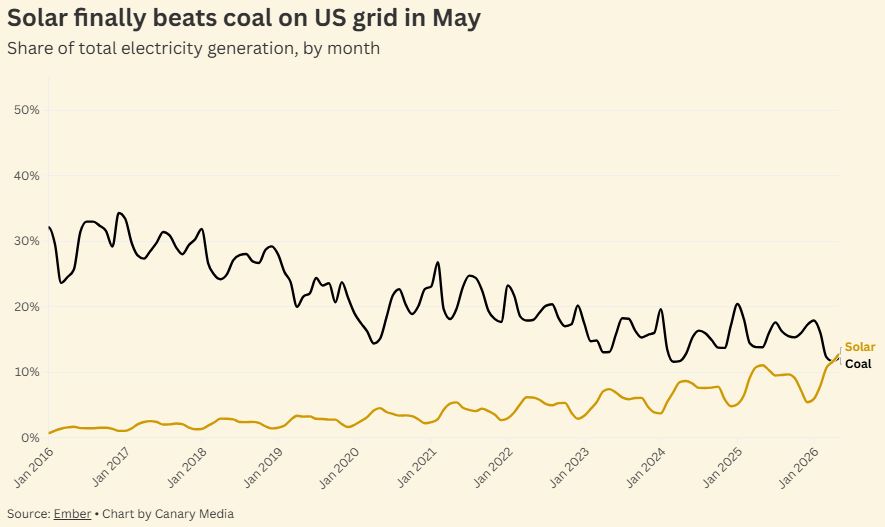

Coal used to make more electricity than any other source in the U.S. Then it fell behind natural gas, and eventually dropped below nuclear. In May, the country’s coal power production slipped behind solar generation, making sunshine the third-biggest source of electricity for the month for the first time.

The U.S. isn’t building more coal plants, though the Trump administration has elected to stop any from closing down, whether or not they can physically operate. Solar, on the other hand, has led the nation in new capacity construction for five years running. When the sun emerges from its wintry slumber, that ever larger fleet shows what it can do.

This upset is all the more striking because, as renewables skeptics love to repeat, solar doesn’t produce all the time. Coal plants can run 24/7, if they aren’t broken or hobbled by uncompetitive operating costs. But even with that structural limitation, solar produced more gigawatt-hours in the daytime than coal did throughout the whole month of May. And this is true not just for a particularly sunny region, or a state with aggressive solar-friendly policies, but across the country.

Solar might not beat coal production for all of 2026, but it’s only a matter of time before it outperforms coal for an entire season, and then eventually for a whole year.

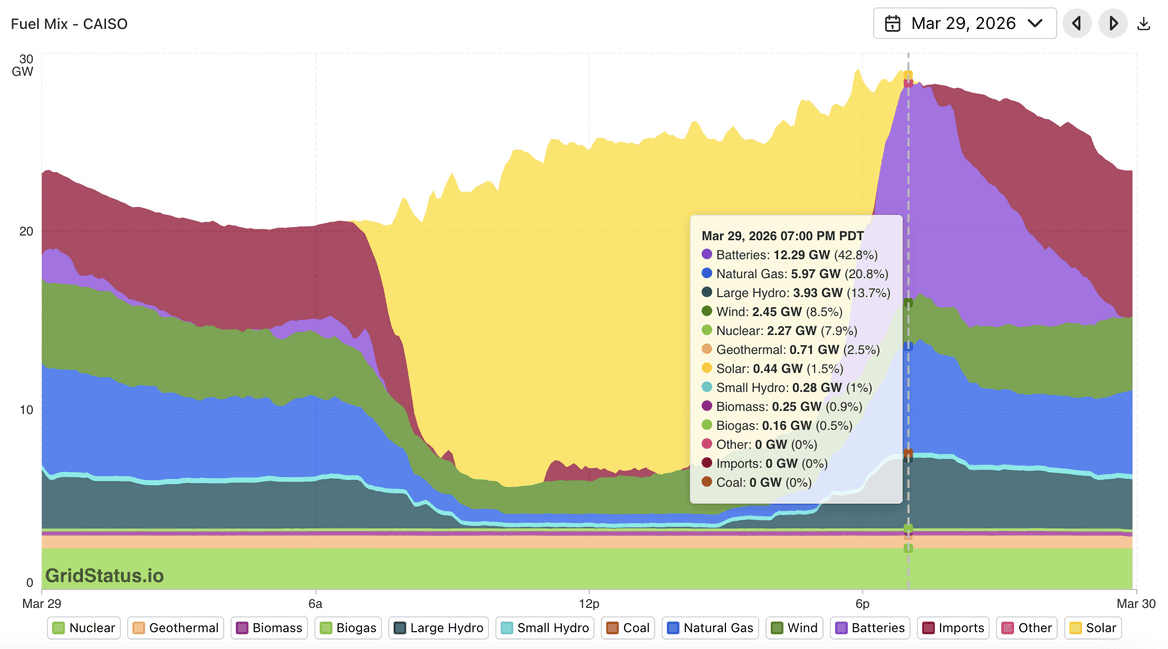

California has entered the execution phase of its energy transition, when the long-promised potential of solar and batteries has turned into empirical breakthroughs in the power markets. The records came at a dizzying pace this spring.

On the evening of March 29, batteries covered 44% of demand (and 42.8% of the supply mix) in the grid managed by the California Independent System Operator (CAISO), which serves about 80% of the state. That was a mild Sunday, so batteries could meet a higher portion of demand than, say, on a blistering hot workday with everyone’s air conditioning turned on. But the absolute numbers speak for themselves: Batteries discharged over 12 gigawatts at 7 p.m. That’s more than New York City consumes on a hot summer day. Not bad for a battery construction spree that largely transpired over the last five years.

On May 16, batteries held gas plants to a shockingly marginal role in the grid for a four-hour period after 7 p.m. Gas never made it above 3% of demand during that time, according to an analysis by the Institute for Energy Economics and Financial Analysis.

The batteries active in California typically can sustain maximum discharge for four hours. This is visible in the daily pattern of grid activity: Batteries surge around sunset to become the single biggest power source in the CAISO grid. Some of them save their energy for later in the night or the early-morning hours before solar produces again. This dynamic leaves a gap in the middle of the night, when gas shows its value.

One way to extend the clean energy success story would be to build longer-lasting batteries. The first major battery with eight hours of duration came online on June 1 in Southern California, and it will offer a sneak preview into what happens when batteries can serve a longer swath of the day.

In the near term, California is tapping more wind power for nighttime supply. The multi-gigawatt SunZia wind farm in New Mexico started shipping power to California this spring, instantly setting new records for wind power’s contribution in the CAISO grid. The Institute for Energy Economics and Financial Analysis compared the grid activity for May 16 of 2025 and 2026. On that day last year, from midnight to 6 a.m., gas generated 3.6 gigawatts, keeping the system going through the night. This year, for that same time period, gas contributed a paltry 560 megawatts. The cheap wind power rushing in from SunZia was pushing gas out of its last redoubt.

One could say these observations are cherry-picking in favor of clean energy. But such ripe cherries simply didn’t exist a year ago, much less five years. California’s clean energy plants should be able to replicate or beat these records in the fall shoulder months. The more challenging test will be whether solar, wind, and batteries can steal market share from gas in the midst of a heat wave, when the fossil fuel has historically hit its maximum output. This El Niño cycle promises to deliver the requisite conditions for that test.

New York state hasn’t built the kind of batteries California has, but it did set a new solar production record on June 3. Solar of all sizes delivered 5.6 gigawatts, serving a record 29% of demand at noon that day, according to the New York Independent System Operator.

The details are more revealing: Almost all of that generation came from small-scale, customer-sited systems, while utility-scale contributed only 530 megawatts. That’s less than the output of individual solar projects out West.

Even the regions that struggle to build much solar are breaking records for themselves. And where you don’t have wide open desert to build sprawling installations, small ones on rooftops and in yards can add up to a meaningful surge.

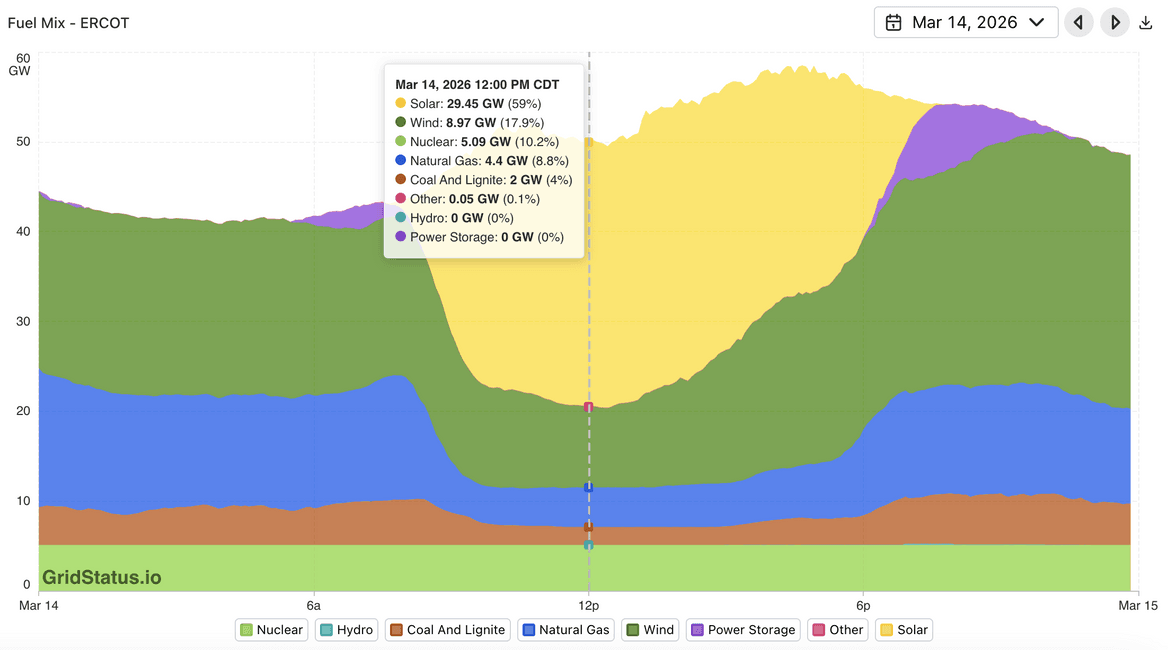

This spring, Texas set just about every clean energy record you could ask for, as helpfully documented by data firm Grid Status.

Batteries shipped the most power to the grid on March 13, at 7:30 p.m., with 10.4 gigawatts, which satisfied a record 20% of evening demand at that moment.

Wind and solar served a record 79% of demand (and 76.9% of supply) on the afternoon of March 14; along with baseload nuclear, the zero-carbon power plants limited fossil-fueled power to just 13% of the fuel mix for a five-hour swath of midday.

The Texas grid produced more solar power than ever before on May 13, a stunning 34.4 gigawatts at 12:40 p.m. It produced more wind power than ever before on May 17, nearly 29 gigawatts at 11:50 p.m. The highest combined renewable output came on May 14 at 3:15 p.m., almost 48 gigawatts.

Again, these are mild shoulder months, when Houstonians aren’t sweltering too much yet and when gas plant operators take their machinery offline for maintenance. In these favorable conditions, we’re seeing what happens when a society unleashes the trifecta of solar, wind, and batteries. The solar peaks at midday; the wind often kicks up after sunset. When a particular day gets both sunny and gusty, the two resources alone now cover most of the midday consumption. And batteries are carving deeper into the evening peaks, corroborating the trend that California pioneered.

No one source of clean energy can run the whole grid on its own, but none has to. The portfolio effect is on stark display as Texas delivers a deregulated version of clean energy abundance.

A yearslong project has finally started producing ammonia with wind power. If the process can be scaled up, it could help ensure farmers have cheap, reliable fertilizer.

In the shadow of a wind turbine on a low rise just outside the western Minnesota town of Morris, a cluster of tanks, pipes, and sheds holds what some believe is the key to a more self-sufficient future for the region’s agriculture and heavy industry.

When the wind is blowing — and it often is, out here — the turbine powers two electrolyzers that cleave hydrogen from water, another system that separates nitrogen out of the air, and a third that binds the two elements to form anhydrous ammonia, a critical input for corn farming. The University of Minnesota West Central Research and Outreach Center commissioned the plant earlier this spring and can produce hundreds of kilograms of homegrown ammonia daily.

As a stable, efficient carrier of hydrogen, the homegrown ammonia could eventually supply raw material for other types of fertilizers, transportation fuels, and high-temperature industrial processes like ironmaking.

“It’s about 100 times cheaper to store and transport ammonia than hydrogen … so this is a gateway for other hydrogen-based industries,” Michael Reese, green ammonia research lead at WCROC, said on a tour of the facility this spring.

“Gateway” is the operative word here. Reese said WCROC plans to add a third electrolyzer to the project in a “future phase,” bringing daily production capacity to about 1 metric ton and annual production between 300 and 400 tons. That sounds impressive, but it’s a rounding error in a highly consolidated industry that produces around 250 million tons of ammonia annually. Minnesota alone imports up to 900,000 tons per year.

That’s a minimum $500 million annual transfer from Minnesota farmers to out-of-state fertilizer suppliers, most of which synthesize the stuff from cheap natural gas at sprawling facilities on the U.S. Gulf Coast, Brandon Isakson, managing director for industry with the St. Paul–based environmental nonprofit Fresh Energy, said in an interview. When prices are high, as they are this year, the outlay can exceed $1 billion, he said.

Anhydrous ammonia and its chemical cousin, ammonium (NH4), join nitrate (NO3) and urea (CO(NH2)2) as the three main nitrogen-derived fertilizers used in modern agriculture — often in combination. All three, along with nonnitrogenous fertilizers like potash and phosphate, are produced in massive “world-scale” plants that put out hundreds to thousands of metric tons daily. They depend on complex global supply chains to reach end users.

Right now, those supply chains are under intense pressure due to the U.S.-Israeli conflict with Iran. About one-third of the world’s urea and one-fifth of its ammonia pass through the Strait of Hormuz, which has been effectively closed to cargo traffic since the beginning of March. While the U.S. has plenty of domestic production capacity, U.S. Department of Agriculture data shows it still imported nearly 40 million tons of various fertilizers in 2025, including nearly 8 million tons of solid and blended urea. Prices for imported urea spiked when the shooting started earlier this year, underscoring domestic farmers’ tenuous relationship with global commodities markets.

Though WCROC has plans to grow the Morris facility, production likely won’t expand there in time to matter for the Hormuz crisis. Nor would it reach the kind of scale that could make a meaningful difference for Minnesota farmers, let alone other hydrogen-hungry industries.

“You’d like to be at 50,000 tons per year to be cost-effective,” Reese said.

But Reese added that he’s optimistic about a not-too-distant future where scaled-up ammonia production facilities dot the Minnesota countryside.

So are others involved with the project. Sameer Parvathikar, senior director of sustainable energy solutions at RTI International, an independent research institute that collaborated with WCROC, said at an April event celebrating the Morris system’s commissioning that it was an important milestone in a multiyear effort to stand up a new, cost-competitive industry from scratch.

“For those of us trying to push this forward from a technology perspective, you realize we have done stuff that actually matters,” he said, noting turnout that included higher-ups in the University of Minnesota system and a North Carolina–based developer looking at commercial applications for an ammonia production pathway that uses clean electricity instead of fossil gas.

At least some farmers here and elsewhere across the Corn Belt see the potential in local ammonia production, too.

In March, a southern Minnesota farming cooperative said it would partner with a Texas-based infrastructure company, a Minneapolis-based carbon credits registry, and the local power and water utility on a project that could produce most of the ammonia its farmers need within a few years. Located in Blue Earth County, the modular plants could pump out as much as 12,000 tons of ammonia annually, the companies said.

It would be one of the first larger-scale deployments of a “modular, green ammonia system that makes the local production and distribution of a critical raw material cost-competitive and more reliable,” according to Talusag, the company behind the technology.

Talusag says its approach lowers ammonia costs by up to 50% by freeing production from fragile global supply chains and using no raw materials other than abundant sun, air, and water. In theory, its plants can locate anywhere with an adequate power supply, whether that’s the middle of farm country or a remote mine site.

KC Graner, president and CEO of Truman-based Central Farm Service, agrees. He told AgWeek in March that farm prices have fluctuated by more than 300% in recent years. Prices can swing several hundred dollars per ton in a single season.

“Local production gives our member-owners a level of control and predictability they’ve never had before,” he said.

Talusag, Central Farm Service, and CleanCounts — the Minneapolis clean energy credits registry — are among more than a dozen members of the Minnesota Made Ammonia Coalition, which pushes for “policy and practical steps” to leverage the work being done at WCROC into commercial-scale green ammonia production.

The coalition’s top priority this year was securing an $8 million legislative grant that the Blue Earth County project’s backers said was needed to move forward. That didn’t happen, leaving its near-term fate uncertain. Tristan Peitz, Talusag’s head of business development, told the House Finance and Policy Committee in April that the facility would have ammonia ready for use in 2028 if it began construction in 2027.

Talusag already operates one green ammonia facility in the Upper Midwest, near the central Iowa town of Boone. Commissioned last spring in partnership with Iowa-based farming cooperative Landus and capable of producing 1 to 2 tons daily, it’s North America’s first “commercial, modular” green ammonia plant, Talusag cofounder and CEO Hiro Iwanaga said at the time. The company is building a plant in Eagle Creek, Iowa, about 50 miles north, that can put out 20 tons daily.

The Boone facility is registered with CleanCounts, which issues a bit more than 40 percent of all renewable energy certificates in North America, chief commercial officer Rob Davis said in an interview. Each certificate, or REC, equals 1 megawatt-hour of electricity, roughly what a typical Minnesota home consumes each month.

To qualify for the federal clean hydrogen tax credit today, producers have to prove that they procured enough renewable power to offset their energy consumption each year. Beginning in 2030, they’ll need to show the power was generated in the same hour it was consumed — a much stricter standard.

“You need a tech-forward registry to be able to meet these requirements,” Davis said.

CleanCounts has dozens of software developers working on a system that can accurately match hour-by-hour output from solar and wind farms across “the vast majority of corn country” by later this year, Davis said.

It’s a big job that’s worth the effort for CleanCounts, which Davis said earns 1 cent when a REC is created and another cent when it’s retired, or claimed by the end user. For cooperatives like Landus and Central Farm Service, the RECs themselves are worth buying because they lower the carbon intensity score, or CI, of their harvests. Biofuels produced from low-CI feedstocks have an easier time qualifying for the federal clean fuels tax credit, state incentives like Minnesota’s sustainable aviation fuel tax credit, and state blending mandates like California’s low-carbon fuel standard.

Lower CI is the impetus for other emissions-reducing investments across the agriculture sector, from pipelines to divert carbon dioxide captured during biofuels production to thermal batteries to replace gas- or coal-powered equipment at ethanol plants. In May, a POET ethanol plant on the Minnesota–South Dakota border commissioned a thermal battery system that charges off the area’s wind-rich power grid, significantly reducing the plant’s reliance on fossil fuels.

Like POET’s battery, and unlike traditional fossil-fueled ammonia factories, green ammonia plants easily flex their output to match variable wind and solar production on the power grid. The WCROC plant can go from 10% to 100% production in about two hours, according to Reese.

Flexible sources of demand on the grid could help Minnesota and surrounding states use renewable power more efficiently. Federal data shows the region’s grid operator curtailed nearly 6 gigawatts of wind power on blustery days — equivalent to six large nuclear reactors — for lack of local demand and transmission capacity.

Minnesota alone would need about 5 gigawatts to produce all its ammonia locally with current technology, according to a 2024 analysis by RMI, an environmental nonprofit. That’s a lot, but maybe not too much. Davis said some projections have curtailment doubling across the region by 2035.

Beth Soholt, executive director for Clean Grid Alliance, a Minneapolis-based nonprofit advocating for clean energy development across the Midwest, said that’s one reason why the region’s policymakers, electric utility leaders, and economic development boosters were enthusiastic about localized green ammonia production just a few years ago.

“Ammonia was the low-hanging fruit, people thought … and you hear every day how expensive the farming inputs are,” Soholt said.

Former President Joe Biden signed legislation authorizing generous tax credits for clean hydrogen production and approved seven regional “hydrogen hubs” to scale and match supply and demand for the stuff. Minnesota was one of several states in the Heartland Hub, where the administration saw abundant wind power supporting a thriving low-carbon fertilizer industry.

The Trump administration has been much less supportive. It ultimately spared the Heartland Hub and four others after earlier moving to dismantle the program, albeit with a shift in focus toward fossil-based production methods. In the meantime, green ammonia boosters’ enthusiasm has been tempered by what Soholt said were “sticky” questions about the cost of electricity and other inputs.

“It just comes down to economics — do these [facilities] pencil out?” she said. “But people have done a lot of work on them.”

For many rural communities and the electric utilities serving them, hope for a green ammonia boom has been replaced by hype around another seemingly endless source of power demand: data centers. Huge computing facilities like the ones Google has proposed near Rochester and Duluth can consume hundreds of megawatts of electricity, many times more than the WCROC and Talusag ammonia plants draw.

Data center loads are less flexible than ammonia plants, however, and they’re attracting increasingly stiff pushback from rural residents concerned about noise, air pollution and other quality-of-life impacts. In addition to being better at soaking up excess renewable power, ammonia plants may be better neighbors, Davis said.

“People are beginning to realize it’s a lot harder to build data centers near wind farms … but there are a lot of farmers growing a lot of corn out near wind turbines, and they definitely need fertilizer,” he said.

While farmers will claim the first batches of homegrown Minnesota ammonia, they’re not the only potential customers. At scale, the industry could provide secure, local supply of a critical input for advanced steelmaking.

Today, most steel plants in the United States use high-grade coal to purify iron in giant, superhot blast furnaces. But those facilities are aging, and eye-watering construction costs mean the U.S. is unlikely to build a new one. So steelmakers are looking ahead to direct reduction, a newer, more flexible process that doesn’t require coal. Most present-day direction reduction plants use natural gas as the reducing agent, but experts say the process can be adapted to run on pure hydrogen.

That could happen here in Minnesota — eventually. Mesabi Metallics, the company behind Minnesota’s first new iron mine in 50 years, says making direct-reduced iron is part of its long-term vision for integrated “green” steelmaking. It’s focused on getting its Iron Range mine open later this year and hasn’t given a firm timeline for a direct-reduction plant, but the prospect is tantalizing for Iron Range boosters hoping to keep the region’s primary industry competitive well into the future.

Reese said that would mark a more sustainable return to form for a state whose early economy was closely tied to the land.

“We have an opportunity here in Minnesota to follow the model we followed in the late 1800s — to take these natural resources and transform these industries,” he said.

Editor’s note: This story is the second in a four-part series on clean energy innovations within Minnesota’s industrial sector. The series is underwritten by Fresh Energy, which like all MinnPost funders does not weigh in on editorial decisions.

Editor’s note: This story was updated on June 9, 2026, to clarify the service provided by CleanCounts, which issues and tracks energy attribute certificates such as renewable energy credits.

This article first appeared on MinnPost and is republished here under a Creative Commons Attribution-NoDerivatives 4.0 International License.

It’s the first time that’s happened across an entire month, and it comes despite the Trump administration’s efforts to reinvigorate coal and hamper solar.

The U.S. just hit a big milestone: It got more power from solar panels than from coal plants in May.

It’s the first time that has ever happened across an entire month, and all the more notable given the Trump administration’s all-out push to revive the moribund U.S. coal industry.

Solar produced 12.8% of the nation’s electricity in May, a sun-soaked month that’s often among the best-performing for the clean energy source, per new data from think tank Ember. Coal power made up just 12.2%, a near all-time low, while natural gas dominated the mix at 37%.

For years, the power sector was the single biggest source of planet-warming pollution in the U.S., which is itself responsible for more historical greenhouse gas emissions than any other nation. America’s heavy reliance on coal, an especially dirty fossil fuel, drove those dubious distinctions.

In the late 2000s, facing hotter competition from increasingly abundant natural gas and a burgeoning renewable energy sector, coal-fired electricity output peaked in the U.S. It’s been all downhill from there for coal, which slipped from providing nearly half the country’s electricity needs two decades ago to just 17% last year. Emissions from the power sector have fallen accordingly, and now it’s the second-largest source in the U.S., after transportation.

President Donald Trump, who has insisted that the words “beautiful, clean” precede “coal” in all instances, is trying his best to stem the sector’s terminal decline. His administration has issued a slew of controversial emergency orders requiring aging coal plants to stay online — even those that are broken or otherwise unable to run. Earlier this month, it announced it would plow $700 million into the industry, both to patch up old plants and to build two new ones.

Coal actually did produce a bit more electricity last year than in 2024, but mostly because a combination of high power demand and elevated natural gas prices made the fuel momentarily more attractive.

Still, that doesn’t reverse the long-term trend. Every year, gigawatts of new clean energy come online in the U.S., because it’s cheap and comparatively easy to build. For several years running, over 90% of new electricity capacity built in the U.S. has been in the form of solar, wind, or batteries.

Meanwhile, the last new coal plant in the U.S. was completed back in 2013.

Take those two facts together, and it’s clear that solar is going to outperform coal many more times in the near future, and by wider and wider margins each time.

.svg)