In the United States, the Trump administration is waging a relentless war on offshore wind, taking an all-of-government approach to thwarting construction of turbines at sea.

On the other side of the Atlantic, however, 10 European countries have formed an alliance to build out 100 gigawatts of offshore wind power and transform the North Sea into what German Chancellor Friedrich Merz called “the world’s largest clean energy reservoir.”

On Monday, officials from Belgium, Denmark, France, Germany, Iceland, Ireland, Luxembourg, the Netherlands, Norway, and the United Kingdom met in Hamburg to sign a declaration vowing to collaborate on construction of enough offshore wind capacity to power nearly 150 million households by 2050. The document, dubbed the Hamburg Declaration, affirms a goal of building a total of 300 gigawatts of offshore wind capacity in the region, although only a third of that would come from international projects that involve cross-border collaboration. The remaining two-thirds would come from national projects built by countries to send power to their own grids.

At least 100 companies signed onto an accompanying industry declaration in which they promise to cut the costs of offshore wind installations and hire upward of 91,000 workers.

“This is a move not just to establish European energy independence, but to support a strategic sector that’s had a very difficult few years,” said Ollie Metcalfe, the head of wind research at the consultancy BloombergNEF.

Europe has faced energy shortages since Russia invaded Ukraine in 2022, forcing Kyiv’s allies to wean themselves off the cheap natural gas the Kremlin had shipped westward for decades. The continent ramped up imports of American liquefied natural gas, but that proved very expensive and has left Europe vulnerable to the Trump administration’s bullying on issues such as Greenland’s sovereignty. Nuclear power produces roughly one-quarter of Europe’s electricity, but building new reactors can take well over a decade and some countries, including Luxembourg, remain firmly opposed to atomic energy. In cloudy Northern Europe, with its limited solar potential, harnessing the fierce gusts on the North Sea with offshore turbines represents one of the best options to produce large volumes of power.

Implementing the pact will prove harder than signing it. Countries with lower electricity prices are likely to encounter pushback over a cross-border compact with nations whose energy-market policies have driven up rates. Norway boasts relatively low electricity prices thanks to its vast system of hydroelectric dams. Already, exports of Norwegian electricity to the continent, where Germany’s decision to shut down its nuclear power plants helped push its rates to some of the highest levels in the world, have stirred political blowback in the Nordic nation.

“Sometimes the technical stuff sounds like the most difficult to overcome, but in reality it’s the political and regulatory barriers that end up being the most difficult to solve,” Metcalfe said.

Norway may contribute the fewest turbines under the pact, BloombergNEF forecasts, because its continental shelf drops sharply into deep water, making it difficult to site traditional turbines bolted to the seafloor. Norway has experimented with floating turbines, but the technology is much less mature. And the country’s offshore energy industry has traditionally focused on oil and gas. (Landlocked Luxembourg, which lacks a shoreline, is contributing financing to the deal.)

Europe’s homegrown offshore wind giants, such as Norway’s Equinor and Denmark’s Ørsted, are likely vendors for the buildout, said Gaurav Purohit, the Germany-based vice president of European asset finance at the credit-ratings agency Morningstar DBRS. With the U.S. government bearing down on projects such as Ørsted’s Revolution Wind in New England and Equinor’s Empire Wind in New York, he said the North Sea buildout would allow the companies to redirect capital back to Europe.

Other likely winners of the offshore wind push include the German utility RWE, German transmission giants TenneT and Amprion, and the French energy giant TotalEnergies, which has committed to a big renewables buildout — a contrarian move among oil majors. While China’s soaring offshore wind companies are looking to enter the European market, “I do think European developers will benefit more,” Purohit said.

But he cautioned that the high cost of building offshore wind, particularly when interest rates are elevated and inflation is driving up the price of materials, means that projects would likely “need financial institutions to take a stake.”

Increasing the transmission connections is key, said Matt Kennedy, an executive who heads up sustainability issues for IDA Ireland, the government agency that attracts foreign investment. Right now, the island nation on the EU’s western fringe is connected to other grid systems only by power lines to the United Kingdom. In 2028, the Celtic Interconnector, a 700-megawatt power line connecting Ireland to France, is set to come online, establishing the first direct transmission between the Emerald Isle and the continent. Kennedy said the two-way line will likely hasten construction of offshore wind in Ireland, where the industry has been stunted by planning bottlenecks and, like Norway, a steep continental shelf dropoff. Ireland, which already has a large onshore wind industry, has 7 gigawatts of offshore turbines approved.

Establishing a link to France “really sets the pace for us to be able to deliver on our commitment,” Kennedy said.

“This is a radical step,” he added. “It’s a massive step for Ireland in terms of providing that enabling architecture to access the European market. This will allow us to export an abundance of renewable energy that we plan to have, but also in times of need allows us to import.”

The pact is not renewable energy for the sake of going green, said Ed Miliband, the British secretary of state for energy security and net zero.

“Our view on offshore wind energy is hard-headed, not soft-hearted,” he said, according to Euronews. “I think offshore wind is for winners. Different countries will pursue their national interests, but we are very clear where our interests lie.”

A decade ago, North Carolina boasted more solar power than any other state in the country but California — a distinction owed to scores of large projects built under a suite of clean energy–friendly policies that the Tar Heel State has since repealed or amended.

Now, many of those solar farms are staring down the end of their initial agreements with Duke Energy, the state’s predominant utility. But under a new proposal before North Carolina regulators, project owners could lock in favorable long-term renewals pending one main condition: They have to add batteries.

The scheme was proffered by Duke and is backed by clean energy businesses and advocates. If it’s green-lit by the North Carolina Utilities Commission, it would represent the first systematic move toward “repowering” large-scale solar facilities in the state. The potential is enormous: Contracts expiring in the next five years total 1.9 gigawatts — an amount equal to more than a quarter of North Carolina’s entire utility-scale solar fleet.

Since battery storage will benefit from federal tax credits with few strings attached for at least another six years, and Duke faces daunting power demands from coming data centers and other large electricity users, this form of repowering could support reliability and affordability. In large swaths of rural North Carolina, extending the life of these older projects also makes more sense than decommissioning them.

“Adding batteries to a system that’s already out there makes it immensely more valuable to the grid,” said Steve Kalland, executive director of the North Carolina Clean Energy Technology Center. “In North Carolina, that’s going to be significant.”

More so than its ample sunshine or abundant open space, state policy propelled North Carolina to become a national solar leader back in 2016.

A decades-old state tax credit supplemented federal incentives, and in 2007, lawmakers adopted a modest but meaningful renewable energy requirement. But perhaps most important was the state’s implementation of a federal law designed to encourage small power producers independent of utility monopolies. North Carolina’s rules under the Public Utility Regulatory Policy Act, or PURPA, were among the most favorable in the country, with standard offer, 15-year contracts available for projects with up to 5 megawatts of capacity.

This cocktail of rules and mandates caused PURPA-qualified solar projects to soar, with over 450 large-scale developments coming online in the state from 2010 to 2017, according to the nonprofit North Carolina Sustainable Energy Association, with a capacity of over 3.3 gigawatts.

But by 2017, Duke was on pace to easily meet the clean energy mandate, and Republican state lawmakers had repealed the tax incentive. What’s more, the utility said the surge in solar was creating interconnection bottlenecks and the need for expensive grid upgrades.

So the company helped draft a new state law that year meant to clear the backlog and move most new solar into a competitive procurement process. The standard offer contracts under PURPA survived but were reduced to 10 years for projects with up to 1 megawatt.

In part due to the PURPA changes, annual solar installations in the state have slowed, dropping from a peak of 985 megawatts in 2017 to an average of just under 500 megawatts in the years that followed.

How much should data centers pay for the massive amounts of new power infrastructure they require? Wisconsin’s largest utility, We Energies, has offered its answer to that question in what is the first major proposal before state regulators on the issue.

Under the proposal, currently open for public comment, data centers would pay most or all of the price to construct new power plants or renewables needed to serve them, and the utility says the benefits that other customers receive would outweigh any costs they shoulder for building and running this new generation.

But environmental and consumer advocates fear the utility’s plan will actually saddle customers with payments for generation, including polluting natural gas plants, that wouldn’t otherwise be needed.

States nationwide face similar dilemmas around data centers’ energy use. But who pays for the new power plants and transmission is an especially controversial question in Wisconsin and other “vertically integrated” energy markets, where utilities charge their customers for the investments they make in such infrastructure — with a profit, called “rate of return,” baked in. In states with competitive energy markets, like Illinois, by contrast, utilities buy power on the open market and don’t make a rate of return on building generation.

Although seven big data-center projects are underway in Wisconsin, the state has no laws governing how the computing facilities get their power. Lawmakers in the Republican-controlled state Legislature are debating two bills this session. The Assembly passed the GOP-backed proposal on Jan. 20, which, even if it makes it through the Senate, is unlikely to get Democratic Gov. Tony Evers’ signature. According to the Milwaukee Journal Sentinel, a spokesperson for Evers said on Jan. 14 that “the one thing environmentalists, labor, utilities, and data center companies can all agree on right now is how bad Republican lawmakers’ data center bill is.” Until a measure is passed, individual decisions by the state Public Service Commission will determine how utilities supply energy to data centers.

The We Energies case is high stakes because two data centers proposed in the utility’s southeast Wisconsin territory promise to double its total demand. One of those facilities is a Microsoft complex that the tech giant says will be “the world’s most powerful AI datacenter.”

The utility’s proposal could also be precedent-setting as other Wisconsin utilities plan for data centers, said Bryan Rogers, environmental justice director for the Milwaukee community organization Walnut Way Conservation Corp.

“As goes We Energies,” Rogers said, “so goes the rest of the state.”

We Energies’ proposal — first filed last spring — would let data centers choose between two options for paying for new generation infrastructure to ensure the utility has enough capacity to meet grid operator requirements that the added electricity demand doesn’t interfere with reliability.

In both cases, the utility will acquire that capacity through “bespoke resources” built specifically for the data center. The computing facilities technically would not get their energy directly from these power plants or renewables but rather from We Energies at market prices.

Under the first option, called “full benefits,” data centers would pay the full price of constructing, maintaining, and operating the new generation, and would cover the profit guaranteed to We Energies. The data centers would also get revenue from the sale of the electricity on the market as well as from renewable energy credits for solar and wind arrays; renewable energy credits are basically certificates that can be sold to other entities looking to meet sustainability goals.

The second option, called “capacity only,” would have data centers paying 75% of the cost of building the generation. Other customers would pick up the tab for the remaining 25% of the construction and pay for fuel and other costs. In this case, both data centers and other customers would pay for the profit guaranteed to We Energies as part of the project, though the data centers would pay a different — and possibly lower — rate than other customers.

Developers of both data centers being built in We Energies’ territory support the utility’s proposal, saying in testimony that it will help them get online faster and sufficiently protect other customers from unfair costs.

Consumer and environmental advocacy groups, however, are pushing back on the capacity-only option, arguing that it is unfair to make regular customers pay a quarter of the price for building new generation that might not have been necessary without data centers in the picture.

“Nobody asked for this,” said Rogers of Walnut Way. The Sierra Club told regulators to scrap the capacity-only option. The advocacy group Clean Wisconsin similarly opposes that option, as noted in testimony to regulators.

But We Energies says everyone will benefit from building more power sources.

“These capacity-only plants will serve all of our customers, especially on the hottest and coldest days of the year,” We Energies spokesperson Brendan Conway wrote in an email. “We expect that customers will receive benefits from these plants that exceed the costs that are proposed to be allocated to them.”

We Energies has offered no proof of this promise, according to testimony filed by the Wisconsin Industrial Energy Group, which represents factories and other large operations. The trade association’s energy adviser, Jeffry Pollock, told regulators that the utility’s own modeling of the capacity-only approach showed scenarios in which the costs borne by customers outweigh the benefits to them.

Clean energy is another sticking point. Clean Wisconsin and the Environmental Law and Policy Center want the utility’s plan to more explicitly encourage data centers to meet capacity requirements in part through their own on-site renewables, and to participate in demand-response programs. Customers enrolled in such programs agree to dial down energy use during moments of peak demand, reducing the need for as many new power plants.

“It’s really important to make sure that this tariff contemplates as much clean energy and avoids using as much energy as possible, so we can avoid that incremental fossil fuel build-out that would otherwise potentially be needed to meet this demand,” said Clean Wisconsin staff attorney Brett Korte.

And advocates want the utility to include smaller data centers in its proposal, which in its current form would apply only to data centers requiring 500 megawatts of power or more.

We Energies’ response to stakeholder testimony is due on Jan. 28, and the utility and regulators will also consider public comments that are being submitted. After that, the regulatory commission may hold hearings, and advocates can file additional briefs. Eventually, the utility will reach an agreement with commissioners on how to charge data centers.

Looming large over this debate is the mounting concern that the artificial-intelligence boom is a bubble. If that bubble pops, it could mean far less power demand from data centers than utilities currently expect.

In November, We Energies announced plans to build almost 3 gigawatts of natural gas plants, renewables, and battery storage. Conway said much of this new construction will be paid for by data centers as their bespoke resources.

But some worry that utility customers could be left paying too much for these investments if data centers don’t materialize or don’t use as much energy as predicted. Wisconsin consumers are already on the hook for almost $1 billion for “stranded assets,” mostly expensive coal plants that closed earlier than originally planned, as Wisconsin Watch recently tabulated.

“The reason we bring up the worst-case scenario is it’s not just theoretical,” said Tom Content, executive director of the Citizens Utility Board of Wisconsin, the state’s primary consumer advocacy organization. “There’s been so many headlines about the AI bubble. Will business plans change? Will new AI chips require data centers to use a lot less energy?”

We Energies’ proposal has data centers paying promised costs even if they go out of business or otherwise prematurely curtail their demand. But developers do not have to put up collateral for this purpose if they have a positive credit rating. That means if such data center companies went bankrupt or otherwise couldn’t meet their financial obligations, utility customers may end up paying the bill.

Steven Kihm, the Citizens Utility Board’s regulatory strategist and chief economist, gave examples of companies that had stellar credit until they didn’t, in testimony to regulators. The company that made BlackBerry handheld devices saw its stock skyrocket in the mid-2000s, only to lose most of its value with the rise of smartphones, he noted. Energy company Enron, meanwhile, had a top credit rating until a month before its 2001 collapse, Kihm warned. He advised regulators that data center developers should have to put up adequate collateral regardless of their credit rating.

The Wisconsin Industrial Energy Group echoed concerns about risk if data centers struggle financially.

“The unprecedented growth in capital spending will subject [We Energies] to elevated financial and credit risks,” Pollock told regulators. “Customers will ultimately provide the financial backstop if [the utility] is unable to fully enforce the terms” of its tariff.

Jeremy Fisher, Sierra Club’s principal adviser on climate and energy, equated the risk to co-signing “a loan on a mansion next door, with just the vague assurance that the neighbors will almost certainly be able to cover their loan.”

Rye Development secured a federal license to build a massive new pumped hydro energy storage facility in Washington state. The company could become the first to construct this type of grid megaproject in the U.S. since 1995.

Long before lithium-ion batteries reshaped the power sector, utilities stored electricity by pumping water uphill when energy was abundant and later letting it descend, turning turbines to generate power when needed. This technique depends on gravity and heavy construction, and the U.S. pumped hydro fleet got built when utilities could unilaterally invest in long-term assets. In the country’s modern, largely deregulated, and rapidly changing power markets, nobody has pulled off the expensive and time-consuming feat.

Until now — potentially. On Thursday, Rye secured a license from the Federal Energy Regulatory Commission to build and operate a planned pumped storage project just north of the Columbia River Gorge, near the town of Goldendale (population 3,500). It’s the final regulatory step, meaning that Rye can now finalize plans and begin building.

“With electricity demand and energy costs on the rise, this type of pumped storage project represents a huge step forward,” said Erik Steimle, director of development at Rye. He added, “It’s a fully domestic source of energy storage: The major components are concrete, steel, and labor.”

That effort joins two others Rye is working on, which Steimle said could start construction sooner: Swan Lake in Oregon and Lewis Ridge in Kentucky. So far, though, none have broken ground.

At Goldendale, Rye plans to excavate two 60-acre reservoirs separated by 2,000 feet of vertical gain. The company will pipe in water from the nearby Columbia River, then circulate the water up and down to store and discharge power.

This will have a nameplate capacity of 1.2 gigawatts, bigger than any battery storage installation thus far. But pumped storage really shines in how long it can discharge power for — in this case, 12 hours. The cost of building a bigger reservoir scales much more favorably than stacking more batteries does to achieve the extended storage.

The project is a bet on increased demand for long-duration storage as intermittent renewable production surges. The Pacific Northwest has built ample solar and wind generation but has struggled to expand its transmission network, which produces congestion on the wires. So a major storage plant like Goldendale could help: charging up when solar or wind floods the network and then discharging back when demand is high.

The project will typically pump water for 12 to 16 hours a day and generate eight hours a day, but it could push that to a maximum of 12 hours, according to the license document.

Individual power plants seldom need to petition FERC for permission, but Goldendale fell under that body’s jurisdiction because it will connect with federal land and pump water from a navigable waterway. Notably, the new reservoirs will not even touch the Columbia, drastically limiting environmental impacts, compared with those from America’s earlier dam-building spree.

The layout covers about 680 acres, largely private land that used to house a decommissioned aluminum smelter, but it connects to transmission infrastructure overseen by the federal Bonneville Power Administration. Up on a ridge, the high reservoir will be nestled among a series of wind turbines. Between that power plant and the smelter, Rye won’t need to build any new access roads, Steimle said.

The approval stipulates certain environmental mitigations: Rye has to schedule its filling of the reservoirs to avoid altering the river flow during salmon smolt migration, for instance; plant native vegetation on disturbed land; and purchase 277 acres elsewhere to dedicate to golden eagles’ nesting and foraging.

With federal permission secured, Rye now needs to lock down customer contracts (much like another capital-intensive long-duration storage project, Hydrostor’s recently approved compressed-air effort in California). This type of infrastructure is too costly to build without a guarantee of revenue. But Rye needed to win its license before it could finalize contracts with customers, Steimle noted. The project can serve utilities in the Pacific Northwest as well as in California, where state regulators have mandated that power providers buy long-duration storage to balance a massive supply of solar generation.

Rye has already secured a financing partner for Goldendale: Danish firm Copenhagen Infrastructure Partners, which also bought Rye’s Swan Lake project, back in 2020. Copenhagen Infrastructure Partners will supply the estimated $2 billion to $3 billion needed to build Goldendale once Rye finds buyers for the clean power.

Now, Rye will finalize construction planning alongside its commercial efforts. The FERC license stipulates that construction must commence within 24 months, so the countdown is on.

Even Rye’s successful licensing journey underscores the challenges of leaning on pumped hydro to support the transition to clean energy. The company filed for its license in June 2020. It took five and a half years to get the green light, and it will take up to two years to finalize plans and then four or five more to actually finish building the thing.

That ponderous pace explains why such a large-scale plant hasn’t been built in the U.S. since the Rocky Mountain Hydroelectric Plant came online in Georgia in 1995. A few other companies have tried, like Absaroka Energy, which is developing the Gordon Butte plant in Montana. Globally, a new pumped hydro site opened in Switzerland in 2022; it took just 14 years.

To put it simply, pumped hydro construction isn’t a nimble response to a rapidly changing electricity mix. Batteries, on the other hand, are — they’re mass-produced in factories and can be installed swiftly in prepackaged containers.

But pumped hydro works extremely well when built. It has a far longer duration than the typical four-hour lithium-ion battery. These facilities also last far longer than lithium-ion cells, which degrade with use. The Goldendale license covers 40 years of operation, but the system is designed to last 100, Steimle said; the owner of the Rocky Mountain plant sought a license extension for another 40 to 50 years.

“Pumped hydro is a battery you can cycle over and over again with little to no degradation over a very long period of time,” he said.

And it clearly works at a massive scale: The U.S. has more than 22 gigawatts already running.

As Paul Denholm, a clean grid modeler at the institution formerly known as the National Renewable Energy Laboratory, told Canary Media previously, “Utilities with pumped-storage plants love them — they’re awesome.”

Since emerging as the world’s No. 2 producer of steel eight years ago, India has ramped up its exports to Europe. By some estimates, upwards of 60% of the country’s steel exports now head to the European Union.

But India’s steelmakers are poised for what one prominent New Delhi–based business magazine recently referred to as a “wake-up call.”

The EU’s world-first carbon tariff — known as the carbon border adjustment mechanism — took effect this month, forcing companies in the bloc to pay levies on certain imports based on how much planet-warming pollution was emitted during their manufacturing. That means metal from Indian steelmakers — which rely heavily on coal — will come in at a much higher price in the EU.

“Europe is the elephant in the room. It’s a pretty big deal,” said Kaushik Deb, executive director of the India team at the University of Chicago’s Energy Policy Institute. “It makes it a lot more urgent for India to start thinking about green steel.”

Coal dominates the steelmaking process in much of the world, and especially in India. The traditional method for producing the metal relies on a coal-fired blast furnace to refine iron ore into iron, which is then forged into steel in a basic oxygen furnace. That two-step process accounts for 43% of India’s steel output, according to a June report from Johns Hopkins University’s Net Zero Industrial Policy Lab.

The rest of the nation’s steel is produced in electric arc furnaces or induction furnaces, alternatives to basic oxygen furnaces that melt iron into steel using electricity. But even that equipment depends on iron refined using coal. The fossil fuel also generates upwards of 75% of the power on India’s grid, meaning that ostensibly cleaner methods that use electricity still generate plenty of emissions.

Some steelmakers in India have begun to build out the infrastructure for direct reduced iron, a cleaner method of making iron than relying on coal-burning blast furnaces. But in contrast to American or European DRI facilities, which typically use natural gas or hydrogen, Indian DRI plants often use coal as the input.

The Indian government has started looking to change the trajectory of its coal use. The fossil fuel is making up less and less of the country’s power mix as India installs record amounts of solar panels and wind turbines and embarks on plans to build new nuclear power stations.

In September 2024, India’s Ministry of Steel — the only cabinet-level agency in any major country dedicated just to steel — issued a 420-page report outlining the potential pathways to greening the industry. The report calls for studies into different approaches to slash emissions from steelmaking, including swapping the coal used in DRI for green hydrogen made with renewables and equipping fossil-fueled facilities with carbon-capture equipment. It also proposes studying ways to retrain workers on greener technologies. But the report acknowledges that financing remains a challenge.

“I don’t see the timeline for this happening optimistically,” said Shreyas Shende, the senior research associate at the Net Zero Industrial Policy Lab who co-authored last summer’s report. “The issue is the pricing. Green hydrogen has no cost competitiveness. The government is running a few pilot projects, but we have to see if it’s scalable.”

Some private companies in India have started their own decarbonization pilot projects. JSW Steel announced plans in 2022 to spend $1 billion on green steel by 2030, and later expanded the vision via a partnership with the South Korean steelmaker Posco to develop a new green-steel mill.

That same year, industrial behemoth Adani inked its own deal with Posco to develop a $5 billion green-steel facility in the western state of Gujarat.

In 2024, Tata Steel entered the green-steel market with plans for a low-carbon mill in the United Kingdom. At the World Economic Forum in Davos, Switzerland, last week, the giant announced another $1.2 billion investment in a green-steel plant in the eastern state of Jharkhand.

Acting on its own, however, the “industry will take a long time to catch up,” Shende said.

“The most important development recently is that the government has talked about putting together a big plan,” he said. “We haven’t seen what that plan looks like. But if and when it does come out, that would have potentially the greatest impact on anything India will do.”

In the meantime, India’s steelmakers — which directly employ 2.5 million workers and generate as much as 2% of the country’s gross domestic product — face increased competition. Last August, a Chinese steelmaker scheduled the first shipment of green steel to Italy, an effort to establish a supply chain between the People’s Republic and the EU ahead of the carbon tariff taking effect. In November, industry groups representing European and Chinese steel producers and buyers came together to work on a uniform set of standards for determining whether steel is, in fact, green.

“The Chinese are much better prepared with green steel than India is, and they will probably gain market share at India’s expense by being more compliant” with the EU’s new carbon tariff, Deb said. “That threat of losing market share is relevant and important for India’s decision-making process. It would be a very hard blow to the Indian steel industry.”

This story was first published by Grist.

One year ago, with one of the first strokes of his presidential Sharpie, President Donald Trump signed an executive order declaring a “national energy emergency,” making good on a campaign promise to “drill, baby, drill.” It was the first of many such orders, signaling that the championing of fossil fuels would be a cornerstone of the new administration: A subsequent order pledged to revitalize America’s waning coal industry, eliminate subsidies for electric vehicles approved by Congress under former President Joe Biden, and loosen regulations for domestic producers of fossil fuels. Yet another executive order withdrew the U.S. from the Paris Agreement, the nearly unanimously adopted international treaty that coordinates the global fight against climate change. He resumed liquefied natural gas permitting paused by his predecessor and reopened United States coastlines to drilling.

In the days following his inauguration, Trump killed a climate jobs training program, closed off millions of acres of federal water designated for offshore wind development, and scrubbed mentions of climate change from some federal agency websites. To many observers, it looked like the most comprehensive reorientation of the executive branch’s environmental and climate priorities in American history.

On paper, it certainly appears as though Trump has continued to make good on these early promises. He pushed Congress to pass the so-called Big Beautiful Bill, which phases out an extensive set of tax credits — for wind and solar energy, electric vehicles, and other decarbonization tools — that were responsible for much of the progress the U.S. was expected to make toward its Paris Agreement commitments. (That move has already led some companies to abandon new clean energy projects.) Trump’s attacks on the nation’s offshore wind industry, which he recently called “so pathetic and so bad,” have been unrelenting, culminating in a blanket ban on offshore leases last month. A few weeks ago, he upped the ante on his earlier withdrawal from the Paris Agreement by severing ties with the United Nations framework that facilitates international cooperation on matters of climate change, environmental health, and resilience — a treaty that was ratified unanimously by the U.S. Senate in 1992.

“It has been an extraordinarily destructive year,” said Rachel Cleetus, climate and energy policy director at the nonprofit Union of Concerned Scientists. It’s not hard to find specific moves that have already done tangible harm to the climate: The EPA, for instance, delayed a requirement that oil and gas operators reduce emissions of methane, an ultra-potent and fast-acting greenhouse gas, for a full year. The Interior Department announced a $625 million investment to “reinvigorate and expand America’s coal industry” and directed a costly Michigan coal plant on the verge of closure to stay open.

However, while these moves have been effective in sowing panic and uncertainty, their long-term effects on the country’s climate policy framework are far from certain. Indeed, only a small fraction of the climate damage threatened by Trump is truly permanent, experts told Grist. That’s not only because many of Trump’s moves may ultimately be ruled illegal — federal judges in Rhode Island, New York, and Virginia, for instance, allowed offshore wind farms in those states to resume construction just last week — but also because executive actions can be reversed by a future president. And the president has not shown much interest in passing energy- or climate-related legislation, a far more durable form of policymaking than executive decree. Despite claims to the contrary, Trump has signed fewer bills than any president since Dwight D. Eisenhower.

“He is not changing law,” said Elaine Kamarck, who worked in the Clinton administration and is the founding director of the Brookings Institution’s Center for Effective Public Management. “He is changing practice.”

Even something as unprecedented as the EPA’s moves to relinquish its own authority to regulate the emissions that affect human health — a responsibility that is a core tenet part of the agency’s mission and is therefore widely regarded as unlikely to hold up in court — could be unraveled by a future administration even if it’s ruled to be legal, though that process would take years.

“You can’t make up for the lost time, the increased emissions, and the extent that new areas are opened up for [fossil fuel] exploration,” said Michael Burger, executive director of the Sabin Center for Climate Change Law at Columbia University. “But from a regulatory perspective, what this administration is doing to EPA and the other agencies are all executive actions that can be undone in the same way they were done.”

The major exception is the GOP’s One Big Beautiful Bill Act, or OBBBA. If a future administration wants to restore expansive tax credits for wind and solar energy, that president will have to push Congress to pass new climate legislation. But the climate-relevant portions of OBBBA are noteworthy for being subtractive rather than additive — and are perhaps more accurately viewed as a representation of Trump’s quest to refute Biden’s legacy than as a desire to radically alter U.S. energy law. Indeed, the new law left in place the tax credits for other sources of carbon-free energy, including nuclear and geothermal — something that more moderate Republicans who do not share the president’s dismissal of climate science have been quick to note.

“We like to point out that the baseload clean energy credits were maintained,” said Luke Bolar, head of external affairs and communications at ClearPath, a think tank that develops conservative climate policies. Sean Casten, a Democratic U.S. representative from Illinois, said that the goal of the Biden-era climate legislation — ensuring that U.S. clean energy can be built in a cost-competitive way — has largely been achieved even if specific parts of the law have been repealed.

“Every single zero-carbon power source … is still cheaper on the margin than a fuel energy source,” he said.

The relative fragility of Trump’s assault on bedrock environmental and climate laws could be a product of the president’s prioritization of political dominance over lasting change, said Josh Freed, senior vice president for climate and energy at the think tank Third Way.

For example, the administration has taken steps to shield the American coal industry from the punishing blows of competition, environmental regulation, and the rising costs of mining. Trump has signed an executive order aimed at “reinvigorating America’s beautiful clean coal industry,” granted coal-fired power plants temporary exemptions from emissions limits, and ended a federal moratorium on coal leasing. But those interventions will do little in the long run to reverse a decline driven mainly by economics: The nation’s aging coal plants are becoming increasingly expensive to run while natural gas and solar energy have only gotten cheaper. And they certainly don’t help the president’s stated goal of reducing household energy costs.

To attempt to make sense of the president’s crusade to save coal is to assume there is a larger political strategy at play — which may not be the case, Freed said.

“There’s no reason to bring back coal other than to show that the administration can bring back coal,” he said. “It’s not like there’s this huge lobbying effort or donor base that will be of significant benefit to MAGA or Republicans if they do it.”

A style of governance motivated by political dominance is a good way to make headlines, but it’s not a particularly effective way to build a lasting legacy. Trump’s efforts to buoy coal may help the industry in the short term, but experts are broadly in agreement that coal can’t be “saved” without sustained support from the federal government. And an industry that can survive only with a coal-friendly Republican in the Oval Office isn’t exactly thriving.

“When you have to get the government to step in to put its thumb on the scale in order to help your industry,” Sean Feaster, an energy analyst at the Institute for Energy Economics and Financial Analysis, told my colleagues earlier this week, “it’s a sign that you’re not particularly competitive, right?”

For decades now, the pendulum of U.S. climate policy has swung left and right, reflecting the priorities of the sitting president. Trump’s climate blitzkrieg may be the starkest example yet of the benefits and drawbacks of that model. But despite his best efforts to stand out from the pack, the president’s first year back in office fits a well-worn pattern. As a result, his victories may not last much longer than his presidency.

For nearly two years, Century Aluminum has been searching for a site to put a giant new U.S. smelter — a decision that largely hinged on where it could strike a deal with utilities to access cheap, reliable electricity.

On Monday, the Chicago-based manufacturer finally unveiled its plans. Rather than build its own power-hungry facility, Century is partnering with Emirates Global Aluminium to jointly develop a smelter near Tulsa, Oklahoma, the companies announced. The facility will be America’s first new aluminum smelter in nearly half a century if completed as planned by the end of the decade.

“Together we will make a huge contribution to rebuilding American aluminum production for the 21st century,” Abdulnasser Bin Kalban, CEO of the Dubai–based EGA, said in a statement.

Century had previously identified northeastern Kentucky as its preferred location for a $5 billion smelter, though the company was also evaluating sites in the Ohio and Mississippi river basins. In 2024, the Biden-era Department of Energy selected Century to receive up to $500 million to build a “green” smelter powered by 100% renewable or nuclear energy.

Century didn’t immediately return Canary Media’s questions about the status of the federal award or how energy issues factored into its decision to join forces with EGA.

But on Tuesday, Century CEO Jesse Gary told Fox Business, “That grant is going to underlie the total investment … to help build this new smelter.”

Aluminum production contributes about 2% of greenhouse gas emissions globally every year, and the majority of those emissions come from generating high volumes of electricity — often derived from fossil fuels — to power smelters.

Emirates Global Aluminium first proposed building its own Oklahoma smelter last May. Up until this week, EGA and Century seemed to be racing each other to fire up their new facilities. The fact that the companies teamed up reflects how difficult it is for manufacturers to secure power at the volumes and prices they need, not only in the United States but globally — a challenge that’s getting even harder with the competition from AI data centers.

Building a smelter “is very expensive and very complicated, so I take it as good news,” said Joe Quinn, who leads the Center for Strategic Industrial Materials for SAFE, which advocates for policies to enhance U.S. energy security.

“There was a scenario where both could have failed,” he added. “But now they’re getting together, and I think that strengthens the likelihood of a new smelter being built in the United States.” He said the news was “a little surprising, but then again not that surprising” given the challenges of opening a multibillion-dollar greenfield smelter.

Under this new agreement, EGA will own 60% of the joint venture and Century will own the remaining 40%. The Tulsa-area facility is expected to produce 750,000 metric tons of aluminum per year, an amount that is 25% larger than previously envisioned — and more than double the current U.S. production of primary aluminum.

A facility that massive will require over 11 terawatt-hours of power, or enough electricity annually to power the city of Boston or Nashville, according to an Aluminum Association report.

America’s output of the versatile metal has sharply declined in recent decades, in large part owing to rising industrial electricity rates. Today, the country operates just four smelters — down from 33 in 1980 — and it imports about 85% of all the aluminum it needs each year. At the same time, the U.S. is using more aluminum in solar panels, power cables, infrastructure, and electronics. By 2035, U.S. demand for primary aluminum is expected to rise by as much as 40%, the advocacy group Industrious Labs said in a report last year.

Annie Sartor, Industrious Labs’ senior campaigns director, said that “two smelters would have been ideal” for boosting U.S. aluminum production. “One is better than none, but neither can succeed without affordable, clean power,” she said in a statement.

Construction on the Oklahoma smelter is set to start by the end of this year, the companies said. Negotiations are still underway with the Public Service Company of Oklahoma, which is a subsidiary of utility giant AEP, and the state of Oklahoma to secure a competitive, long-term power contract.

Last year, EGA signed a nonbinding agreement to build its proposed smelter with the office of Republican Gov. J. Kevin Stitt, a deal that includes over $275 million in incentives, including discounts for power. Oklahoma’s “energy abundance” was a key factor in selecting the state for the new aluminum smelter, Simon Buerk, EGA’s senior vice president for corporate affairs, previously told Canary Media.

More than 40% of Oklahoma’s annual electricity generation comes from wind turbines spinning on open prairies, while about half the state’s generation comes from fossil-gas power plants. Last summer, the Public Service Company acquired an existing 795-megawatt gas plant south of Tulsa to meet the rising energy needs of its customers, potentially including EGA.

Buerk said last year that the Oklahoma smelter’s annual power mix “will be based on EGA’s decarbonisation objectives, market dynamics, and market demand for low-carbon aluminum.” He confirmed that Monday’s announcement doesn’t change any of the options being discussed in ongoing negotiations with the utility. That includes a potential tariff structure that gives the smelter dedicated long-term access to a proportion of renewable energy.

The news that Century Aluminum is investing in Oklahoma comes as a major letdown for some environmental and labor groups in Kentucky, who had advocated for bringing the project to their state. Century already owns two aging smelters in western Kentucky, and the new facility was supposed to create thousands of construction jobs and more than 1,000 permanent positions — jobs that will now go to Oklahoma.

“This is a disappointing loss for Kentucky, but it should serve as a wake-up call,” Lane Boldman, executive director at Kentucky Conservation Committee, said in a statement. “For Kentucky to remain an energy leader and meet the needs of industries looking for reliable and affordable power, it must modernize its energy infrastructure more quickly, such as grid modernization, energy storage, and diversifying with renewables.”

An update was made on Jan. 27, 2026 to include a response from EGA and comments from Century CEO Jesse Gary.

Home-electrification startup Jetson just raised $50 million to fuel its ambitious effort to slash the cost of installing heat pumps in the U.S. and Canada.

Founded in 2024, Jetson says it can install the ultraefficient appliance for 30% to 50% less than competitors. The company has also developed its own smart heat pump, called the Jetson Air, which it unveiled last September. Currently, the startup operates in its home base of British Columbia, Canada, and in Colorado, Massachusetts, and New York, with over 1,000 heat-pump installations to date.

Jetson’s team, which has grown from 75 employees in September to 120 today, has extensive experience in designing consumer hardware. Co-founder and CEO Stephen Lake previously led smart-glasses startup North, which Google acquired in 2020. Several former North employees have joined Lake to work on home-electrification products.

The infusion of Series A funding will help Jetson continue to grow its team — and its market reach.

Jetson will use the investment to develop other home appliances, find ways to further reduce costs for consumers, and expand into new geographies, Lake said. The company plans to unveil a heat-pump water heater midyear.

As for geographic expansion, Jetson will prioritize regions where “the need for efficient heating is clear,” he said. “We’ll be in Washington state shortly and will be announcing new locations throughout the year.”

Funders flocked to the company in part because Jetson is pursuing “an absolutely massive market,” according to Ryan Gibson, an investor at Eclipse Ventures, which led the funding round. Roughly half the homes across the U.S. and Canada burn fossil fuels for heating, according to government data, and could switch to emissions-free heat pumps.

The market for the heating-and-cooling appliance is ripe for disruption, according to Gibson. The way that heat pumps are traditionally sold and installed is fragmented and low-tech, with little pricing transparency, he said. Contractors typically need to perform assessments in person in order to provide an estimate. By contrast, Jetson provides instant quotes online and at competitive prices that rival the cost of a furnace plus a conventional air conditioner.

On average, a Jetson system costs about $15,000 before local incentives, Lake said. That’s quite a departure from the national average. Using 2024 data, nonprofit Rewiring America estimated that for a medium-size home, a central heat-pump system costs a median of $25,000. (Jetson declined to share whether it’s currently profitable.)

To achieve those lower prices, Jetson takes a vertically integrated approach: from designing its software-enabled and sensor-equipped heat pump to having its own technicians roll up in one of the startup’s green electric trucks to install the appliance in a person’s home. The company also provides ongoing remote monitoring so that it can alert customers to quiet issues, like a dirty air filter that’s eroding performance.

In addition to Jetson, venture capitalists have backed a few other “heat-pump concierge” startups in recent years, though more modestly. Elephant Energy raised $3.5 million in seed funding in 2022; Tetra secured $10.5 million in seed money in 2023; and Quilt, which makes mini-split systems, added to a $33 million Series A with a $20 million Series B round in December.

Jetson’s funding round comes just after the U.S. government repealed a $2,000 tax credit for heat pumps, as well as subsidies for other efficiency upgrades, and as the nation struggles with rising energy bills. This presents a clear opportunity for firms like Jetson, which promise big cost savings over traditional installers. And with the new cash, the startup has a chance to deliver.

See more from Canary Media’s “Chart of the Week” column.

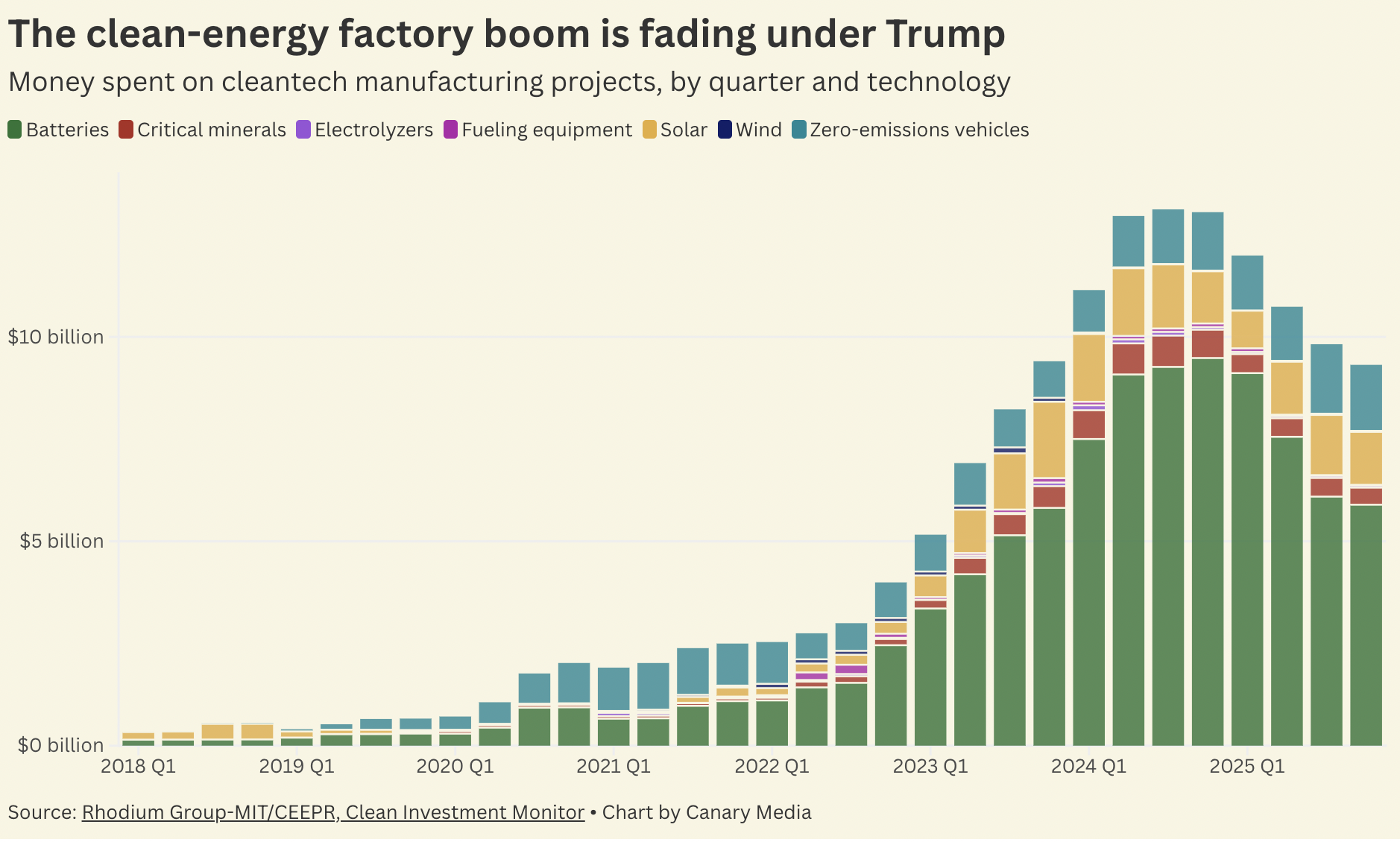

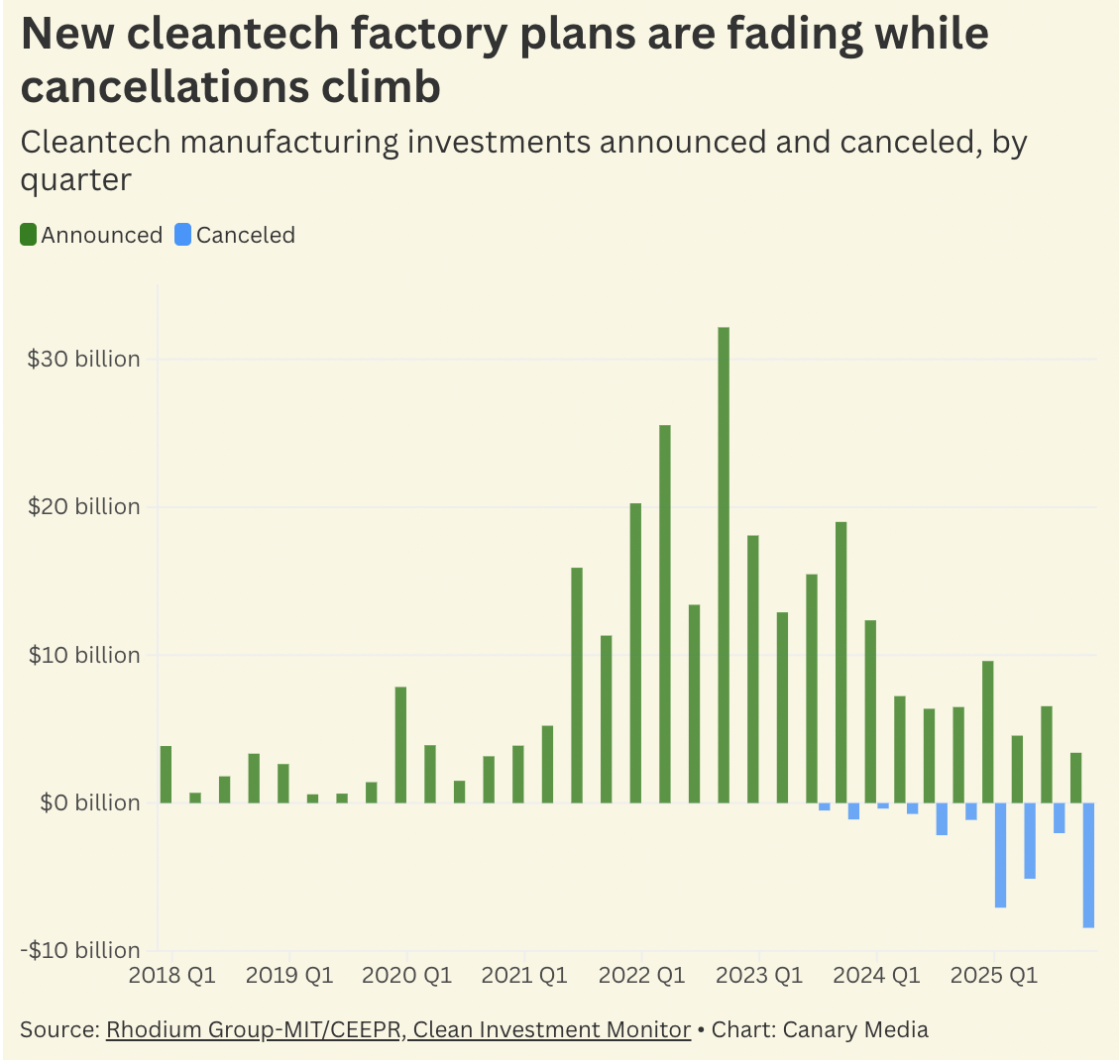

Clean energy manufacturing was on the upswing in the U.S. Then the first year of Trump 2.0 happened.

After years of increasing investment in factories to make batteries, electric vehicles, solar panels, and more — a surge prompted by the Inflation Reduction Act — the trend reversed under the Trump administration last year. Companies spent a total of $41.9 billion on cleantech manufacturing facilities in 2025, down from $50.3 billion the year before, per fresh figures from the Clean Investment Monitor, a joint project from Rhodium Group and the Massachusetts Institute of Technology’s Center for Energy and Environmental Policy Research.

More concerning, however, is the fact that businesses are making fewer new plans to invest in cleantech factories — and a whole lot of companies are backing out of prior commitments.

Cancellations nearly matched factory announcements last year: Firms unveiled a total of $24.1 billion in new cleantech manufacturing projects, but scrapped $22.7 billion worth.

It’s a dramatic reversal. The Biden-era Inflation Reduction Act had spurred well over $100 billion in cleantech manufacturing commitments through incentives for both factories and their customers, be they families in the market for an EV or energy developers building a solar megaproject. The ensuing boom in cleantech factory construction created thousands of jobs and caused overall manufacturing investment to soar. Most of the investment was planned for areas represented by Republicans in Congress.

But last year, the Trump administration put strict stipulations on incentives for factories and repealed many of the tax credits that helped generate demand for American-made cleantech. It also showed an astonishing hostility to clean energy projects — namely offshore wind — and cast a general cloak of uncertainty over the entire economy.

To be fair, other potential factors are at play.

Some of the slowdown in cleantech factory investment could simply be the market maturing. Plenty of projects announced right after the Inflation Reduction Act might already be online, or close to it. Or it could be the result of the gravitational pull of the data center boom, which is attracting gobsmacking amounts of capital that could have otherwise financed more cleantech factories.

But either way, as the new data shows, the Trump administration has weakened the case for investing in expensive projects tied to clean energy. I’m willing to bet that the consequence will be more factory cancellations — and less investment — over this year, too.

This analysis and news roundup come from the Canary Media Weekly newsletter. Sign up to get it every Friday.

When it comes to state politics, 2026 is already in full swing. As legislators reconvene and new governors are sworn in, it’s becoming clear that leaders will focus on one energy issue in particular this year: affordability.

While last year’s elections didn’t bring any major changes to the White House or Congress, skyrocketing energy prices played an undeniable role in propelling Democrats to victory in state elections across the country.

Take a look at New Jersey, where Democratic Gov. Mikie Sherrill was sworn in this week after campaigning on a promise to lower power prices while building out clean energy. She took her first steps in that direction on Tuesday, signing executive orders to accelerate solar and storage development, consider freezing electricity rate hikes, and expand utility bill credits for customers.

Those credits will be funded in part by the Regional Greenhouse Gas Initiative, an East Coast carbon market that saw good news with the inauguration of Virginia Democratic Gov. Abigail Spanberger this past weekend. Spanberger is already moving to rejoin RGGI, with an assist from the state’s Democratic-controlled legislature, after the previous Republican governor pulled Virginia out of the program back in 2023. On her first day in office, Spanberger also directed state agencies to find ways to curb energy and other household costs.

Affordability is sure to continue to dominate politics this year in Virginia, also known as the data center capital of the world, clean energy advocates recently told Canary Media’s Elizabeth Ouzts.

“Oftentimes, I go into a legislative session sort of just guessing what people are going to care about,” said Kendl Kobbervig of Clean Virginia. Not this year.“No. 1 is affordability, and second is data center reform.”

Massachusetts’ legislature shares that priority, reports Canary Media’s Sarah Shemkus. But even though the statehouse remains firmly in Democratic hands, lawmakers aren’t aligned on how to curb costs in the long term. Some are targeting volatile natural gas prices and the cost of replacing aging pipelines, others say clean energy and transmission construction are to blame, and still others are homing in on utility profit margins.

The reality is that the energy affordability crisis isn’t a problem with just electricity prices or natural gas prices; both are rising at rates higher than inflation across the country. And so it’s going to take strong, and perhaps creative, solutions to keep them in check.

Trump’s year of energy upheaval

It’s been a year since President Donald Trump took office for the second time, and there’s been no shortage of energy-industry shake-ups in the months since.

On his first day in office, Trump called out rising power demand and declared a national emergency on energy, which he has since used to justify keeping aging coal plants open long past their retirement dates.

His signature spending law, the One Big Beautiful Bill Act, gutted tons of clean energy tax incentives. And that’s not to mention the administration’s decarbonization funding clawbacks, its holdup of renewables permitting, and its relentless attacks on the nation’s offshore wind industry.

Trump’s year-two agenda is already starting to take shape. Expect to see his administration order more coal plants to stay open, cancel additional clean energy funding, and throw up hurdles we can’t even imagine yet.

Geothermal is having a moment

As clean energy sources like offshore wind and solar struggle to snag a foothold in the new, post–tax credit world, geothermal proved this week that it still has the juice.

A wave of announcements from pioneering geothermal startups began on Wednesday, with Zanskar announcing it had raised $115 million in a Series C funding round. It’ll use the infusion to expand its AI software, which it used to uncover an untapped, invisible geothermal system in Nevada last year. Also on Wednesday, Sage Geosystems announced a more than $97 million Series B round, which will fund its first commercial-scale power generation project, slated to come online this year.

Fervo Energy completed the trifecta as it quietly filed for an IPO, Axios Pro reported on Thursday. The company hasn’t shared details about the filing, but said in December that it had raised about $1.5 billion so far in its quest to build a massive enhanced geothermal system in Utah.

Back to work: Wind farms off the coasts of New York, Rhode Island, and Virginia have all restarted construction after legal wins last week against the Trump administration’s stop-work order, though two other projects remain paused. (Canary Media)

Solar keeps surging: An Energy Information Administration analysis finds utility-scale solar is the fastest-growing power generation source in the U.S., and will continue to expand through 2027 as the shares of coal and gas in the energy mix decline. (EIA)

Rural resilience: North Carolina towns devastated by 2024’s Hurricane Helene are installing solar panels and batteries at community hubs to prepare for future disasters, with help from a program that could become a national model. (Canary Media)

Clean-steel influencers: A new report shows automakers buy at least 60% of the primary steel made in the U.S., which gives them leverage to push steelmakers to clean up production. (Canary Media)

Batteries at breakfast: A Brooklyn bagel shop is cutting its power bills by using suitcase-size batteries to run its oven and fridges when electricity demand is high. (Canary Media)

Renewables’ European win: Wind and solar generated 30% of the EU’s electricity last year, while fossil fuels provided 29%, marking the first time renewables have beaten coal, oil, and gas. (The Guardian)

Clawback consequences: Some communities that lost federal climate grants last year have sued to reclaim them, while others have had to move on from projects that would’ve helped them curb pollution and adverse health effects. (Grist)

.svg)